The Institutional Evolution of Tokenized Assets and On-Chain Infrastructure

This chapter summarizes the relationship between stablecoins, liquidity networks, and DeFi credit structures, outlines the overall framework of on-chain finance, and discusses potential long-term integration paths with the traditional financial system.

I. Shift in Focus: From Stablecoins to Real-World Assets

In previous lessons, we discussed the credit structure of stablecoins, on-chain lending and liquidation mechanisms, and their structural comparison with traditional finance. A natural question arises: once stablecoins become the unit of account and settlement tool on-chain, can the on-chain system support a wider range of asset types?

Tokenized assets are not a new concept, but as stablecoin networks mature, their institutional significance changes. Stablecoins provide a unified unit of account and liquidity foundation, enabling on-chain assets to go beyond native crypto assets and map real-world bonds, fund shares, and cash-like instruments.

The core issue is not technical, but rather how the credit pathway extends.

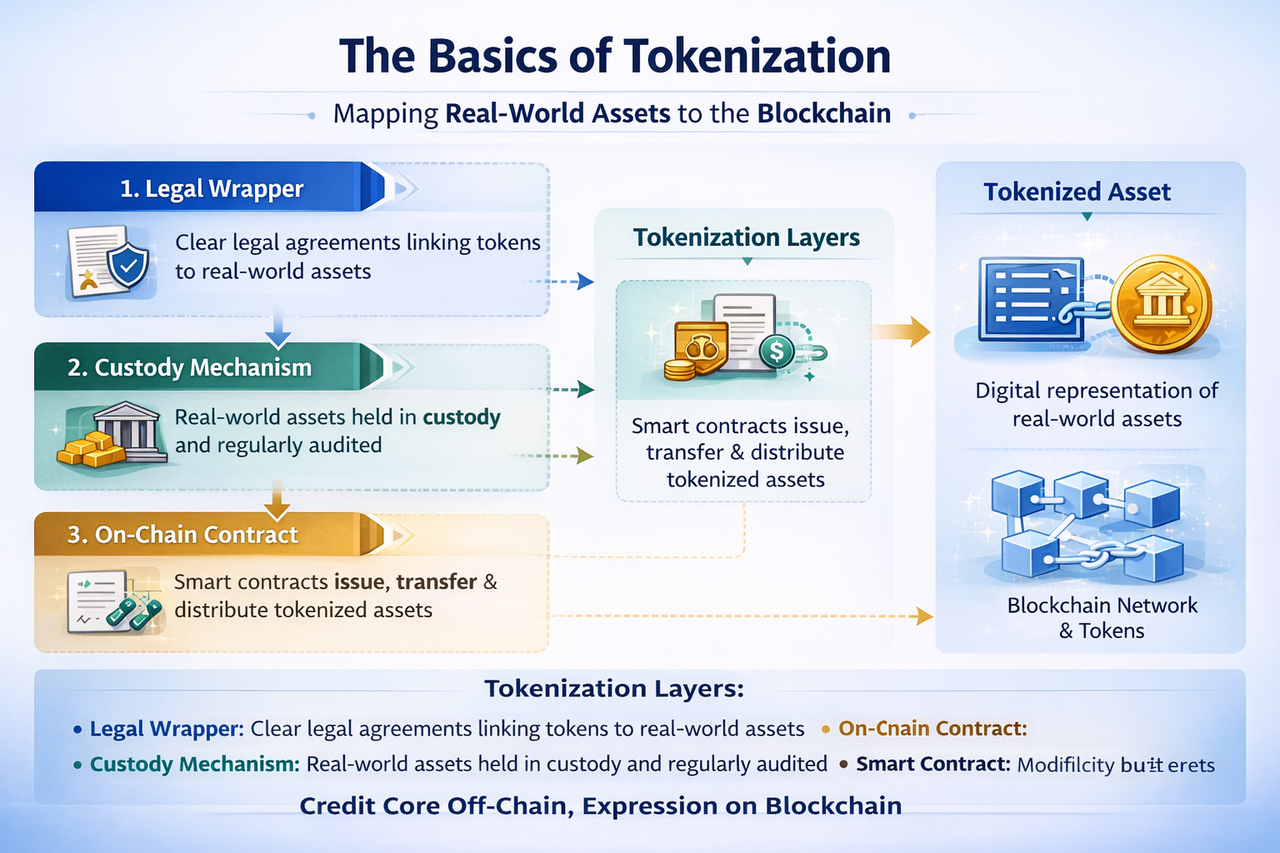

II. The Basic Logic of Tokenization

Tokenization refers to mapping the ownership or income rights of real-world assets onto the blockchain through legal structures and technical interfaces, allowing them to be transferred and settled within blockchain networks.

This structure typically consists of three layers:

Legal vehicle: Ensures a clear ownership relationship between the on-chain token and the real-world asset

Custody mechanism: Ensures the underlying asset actually exists and is auditable

On-chain contract: Facilitates token issuance, transfer, and income distribution

Unlike early crypto assets, the credit core of tokenized assets remains off-chain. The on-chain system is responsible for expression and circulation, not for creating the asset itself.

III. RWA: On-Chain Mapping of Real-World Assets

In recent years, “RWA (Real World Assets)” has become an important expansion direction for on-chain finance. Representative forms include on-chain versions of short-term government bond funds, money market fund shares, and corporate debt certificates.

For example, BlackRock’s on-chain fund products and Franklin Templeton’s fund shares issued on blockchain demonstrate the trend of traditional asset management institutions entering on-chain structures.

This phenomenon reflects two changes:

On-chain systems are gradually gaining institutional recognition

Stablecoin networks provide the settlement foundation for real-world asset circulation

In this structure, stablecoins play the role of payment and settlement, while tokenized assets provide yield and investment opportunities. The combination forms a preliminary structure for on-chain capital markets.

IV. Institutional Advantages and Real-World Constraints

The potential advantages of tokenized assets include:

Improved settlement efficiency with fewer intermediary layers

Enhanced asset transparency

Reduced friction in cross-border circulation

Support for smaller unit splits of shares

However, real-world constraints remain clear:

Legal ownership must be recognized across different jurisdictions

Investor compliance checks are still required

Custody of underlying assets still relies on traditional institutions

Tax and accounting rules are not yet unified

This means that on-chain infrastructure does not eliminate institutional costs but changes their distribution. Technology can optimize processes but cannot replace legal systems.

V. Infrastructure Upgrade: From Public Chains to Permissioned Networks

As institutional participation increases, infrastructure structures are also evolving. Early on-chain finance was mainly based on open public chain networks. With institutions entering, there is greater focus on compliance and permission control.

For example, JPMorgan Chase’s Onyx platform and certain consortium chain structures emphasize permissioned access and identity verification mechanisms. These networks retain the programmability of blockchain while embedding compliance and audit modules.

Two paths can be observed in parallel:

Open public chains continue to support decentralized protocols

Permissioned or hybrid chains support institution-grade assets

In the future, interface layers may emerge to connect both types of networks, with stablecoins or deposit tokens serving as bridges.

VI. Changes in Yield Structure

When real-world assets move on-chain, yield structures change. In traditional finance, asset income distribution is usually handled by registrars and custodian banks. In an on-chain structure, income can be automatically distributed to holder addresses via smart contracts.

This brings two effects:

Income distribution becomes more transparent and automated

Investors gain a more direct understanding of asset cash flow structures

However, it also requires stricter contract audits and risk controls. Contract errors can directly impact income execution, making technical risk a new institutional variable.

VII. Reassessing Risk Structure

Tokenization does not eliminate risk but introduces new categories:

Legal risk: Whether on-chain tokens are legally enforceable

Technical risk: Smart contract vulnerabilities or network attacks

Liquidity risk: Insufficient market depth on-chain

Regulatory risk: Shifts in policy stance

Therefore, the maturity of on-chain infrastructure is reflected not only in technical stability but also in legal and regulatory coordination.

VIII. From Tools to Networks

When stablecoins provide settlement foundations, tokenized assets offer investment targets, and on-chain lending supplies credit expansion tools, a more complete financial network begins to take shape.

This network has three features:

Unified unit of account

Automated settlement mechanisms

Programmable asset structures

It does not entirely separate from traditional finance but rather adds a new technology layer atop existing institutional frameworks. On-chain finance is gradually shifting from a collection of single tools to a sustainable network of assets and credit.

IX. Lesson Summary

The emergence of stablecoins has transformed blockchain from a mere record-keeping technology into one that fulfills functions closer to financial systems. From the initial on-chain unit of account, to the core medium for cross-chain liquidity, and then to the principal foundation within DeFi credit structures, stablecoins have gradually evolved into the monetary layer of on-chain finance.

Reviewing this course’s structure shows that on-chain finance is not a single technological innovation but a system composed of multiple layers of infrastructure:

Monetary layer: Stablecoins provide a unified unit of account and settlement medium, enabling on-chain assets to circulate under unified standards.

Liquidity layer: DEXs, cross-chain bridges, and liquidity pools connect stablecoins to various protocols and networks, forming composable capital networks.

Credit layer: Lending protocols, interest rate markets, and automated liquidation mechanisms generate on-chain credit based on stablecoins.

Asset layer: RWAs and tokenized assets bring real-world assets on-chain, gradually expanding the financial system’s coverage.

Compared with traditional finance, the core difference in on-chain finance is not just “decentralization” but rather the way infrastructure is organized. Traditional finance relies on banks, clearinghouses, and payment networks as multi-layer intermediaries, while on-chain finance breaks these functions down into composable protocol modules. Clearing, settlement, lending, and trading all take place within the same ledger environment, resulting in greater transparency and automation.

At the same time, stablecoins are gradually becoming an important connection point between traditional and crypto finance. On one hand, most stablecoins still rely on real-world assets as reserves—drawing their credit base from traditional financial systems; on the other hand, stablecoins form new liquidity networks on-chain, enabling capital to flow globally at lower costs.

This dual structure means that the development of on-chain finance is not simply a replacement for traditional finance but more likely a fusion and restructuring at the infrastructure level. In future financial systems, some functions will remain with traditional institutions—such as asset custody, compliant issuance, and credit endorsement—while others may run as protocols on-chain—such as trade matching, settlement, and liquidity management.

With regulatory frameworks becoming clearer, continued entry by institutional investors, and growth in RWAs and tokenized assets, the role of stablecoins may further expand—from initial transaction medium to global payment tool to core settlement asset in on-chain finance—its importance is steadily increasing.

Thus, stablecoins can be seen as a key institutional starting point: they not only solve pricing issues in crypto markets but also provide a sustainable monetary foundation for on-chain finance. Based on this foundation, financial activities such as lending, derivatives, asset tokenization, and cross-border payments can gradually unfold—ultimately forming a more open, programmable, and globalized financial network.

Lesson 1:The Essence of Stablecoins—On-Chain Mapping of the US Dollar

Lesson 2:From Stablecoins to On-Chain Dollar Networks

Lesson 3:From Stablecoins to On-Chain Credit: The Formation of Interest Rates and Lending Structures

Lesson 4:On-Chain Finance vs. Traditional Finance: Structural Comparison and Boundary Redefinition

Lesson 5:The Institutional Evolution of Tokenized Assets and On-Chain Infrastructure

Related Courses

The Beginner's Guide to Blockchain-based Airdrops

Crypto Mining Equipment

Learn about web3 data and analytics

Identity in Crypto: Main Projects

Crypto Mining