From Stablecoins to On-Chain Dollar Networks

This chapter analyzes how stablecoins evolve from settlement tools into on-chain dollar networks, forming a liquidity system that spans multiple chains and protocols, through the three-layer structure of issuance, circulation, and application.

I. Problem Transformation: From Single Asset to System Structure

In Lesson 1, we defined stablecoins as on-chain settlement layer assets—a foundational tool for settlement and valuation. This definition highlights their functional attributes but does not yet address structural aspects. This lesson raises a further question: As the scale of stablecoins continues to grow, their circulation paths extend, and application scenarios become richer, do they remain merely “utility tokens,” or have they evolved into a relatively independent dollar circulation network?

The key issue is not growth in quantity, but structural evolution. When an asset simultaneously encompasses issuance mechanisms, settlement pathways, and financial applications—and forms an internal cycle among these three—its nature changes. It ceases to be a single-point product and becomes part of a network structure.

Stablecoins are undergoing this transformation. While they have not separated from the real-world financial system, their operational mechanism now exhibits a new organizational model—a dollar distribution and settlement network operating on blockchain ledgers.

Understanding this is the prerequisite for understanding on-chain financial structures.

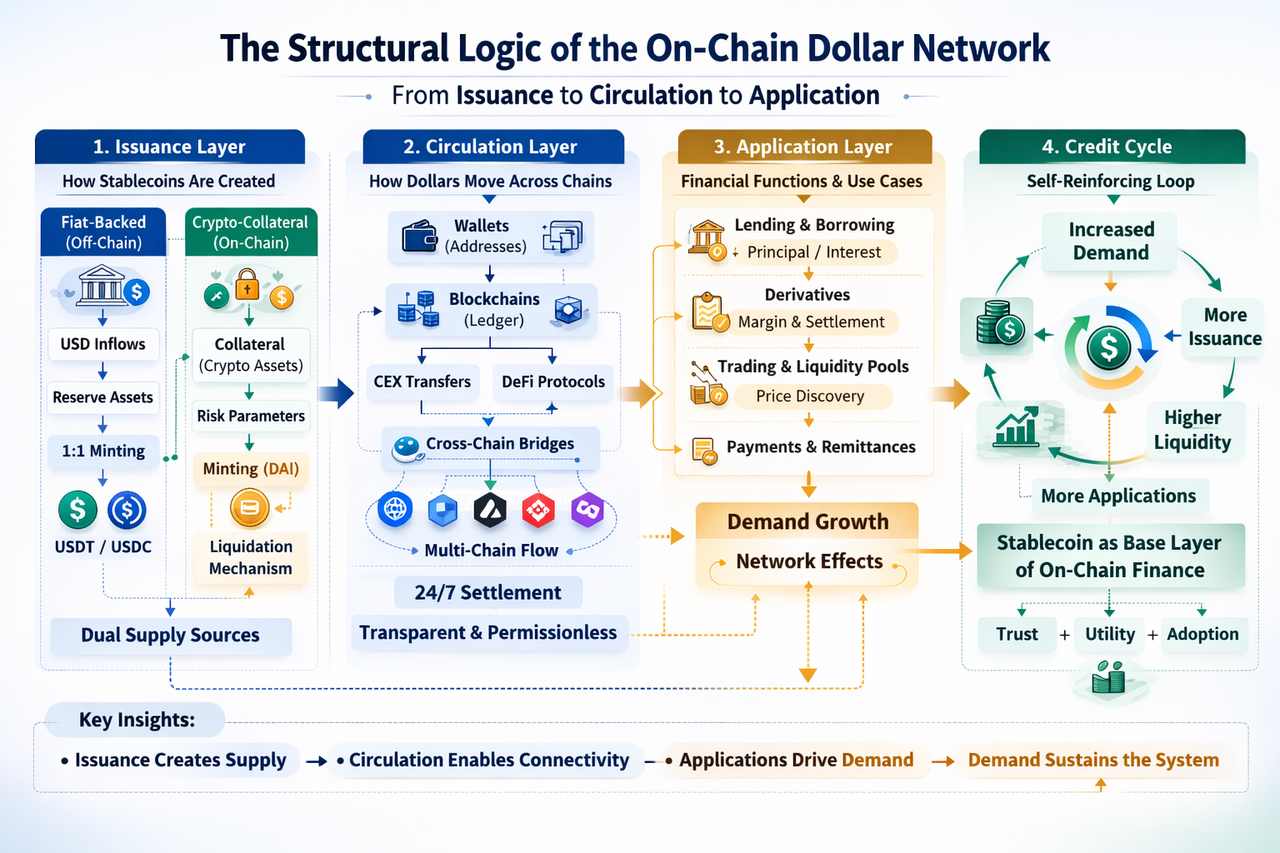

II. Issuance Layer: The Generation Mechanism of On-Chain Dollars

The starting point of any currency network lies in its issuance structure. Fiat-backed stablecoins represented by Tether’s USDT and Circle’s USDC are generated based on a mapping relationship between “off-chain assets—on-chain minting.”

The basic process is: receive USD or equivalent assets off-chain → record reserve assets → mint equivalent tokens on-chain

This structure has three institutional features:

On-chain supply is tied to the scale of off-chain assets.

Minting and redemption mechanisms form supply-demand adjustment channels.

The structure of reserve assets affects overall credit stability.

Structurally, this is equivalent to embedding a “dollar interface” within the blockchain system. Issuing institutions act like settlement nodes, but the credit foundation still comes from traditional financial assets.

Another path comes from crypto-collateralized stablecoins, such as DAI launched by MakerDAO. Their issuance logic does not rely on external fiat inflows, but is based on on-chain asset collateralization and automated liquidation mechanisms.

Its supply expansion depends on:

Collateral asset scale

Risk parameter settings

Liquidation thresholds and stability fees

This means that partially self-circulating structures emerge within the on-chain dollar network—generating liquidity without off-chain capital inflows.

Thus, at the issuance layer, the on-chain dollar network presents dual sources:

External input (fiat reserves)

Internal collateral (on-chain asset generation)

These two paths together form the foundation of stablecoin supply and create different credit structures.

III. Circulation Layer: Cross-Platform and Cross-Chain Dollar Transfer Structures

If issuance determines “generation,” circulation determines “connection.”

The key for stablecoins to truly form a network lies in their transfer pathways no longer relying on a single bank settlement system, but instead achieving peer-to-peer accounting via blockchain.

Wallet addresses become account units; public chains become settlement ledgers.

In practice, the stablecoin circulation structure consists of multiple levels:

Asset transfers between centralized exchanges;

Liquidity pools in decentralized exchange protocols;

Cross-chain bridges and multi-chain deployment structures;

OTC trading and on-chain payment scenarios.

When stablecoins are deployed across different public chains and maintain their pegged relationships, on-chain dollars are no longer limited to a single network but form a cross-chain circulation system.

This system has two core features:

Settlement operates continuously.

Transfer paths are open and transparent.

Compared with traditional banking systems, its settlements are not restricted by business hours nor dependent on centralized clearing nodes. The expansion of the circulation layer brings about “network externalities.”

The value of stablecoins comes not only from reserve assets, but also from their acceptability and frequency of use. When an asset is widely accepted as the default unit of account, it gains structural status.

IV. Application Layer: Stacking Financial Functions and Credit Cycles

Issuance provides supply; circulation provides connection; but what truly determines the status of stablecoins is the application layer.

When on-chain lending, derivatives, market making, and yield protocols commonly use stablecoins as units of account, their role fundamentally changes.

In lending protocols, stablecoins typically serve as principal or valuation assets;

In derivatives markets, stablecoins serve as margin and P&L settlement units;

In liquidity pools, stablecoins pair with volatile assets to form the basis for price discovery.

When most protocols default to using stablecoins as benchmark assets, the interest rate structure and yield curves of on-chain finance begin to revolve around stablecoins.

This results in three changes:

On-chain credit expansion starts with stablecoins;

Financial activities form cycles around stablecoins;

Demand is driven not just by trading, but by financial functions.

At this point, stablecoins become the foundational layer of the credit system rather than an auxiliary tool. The deepening of the application layer enables the on-chain dollar network to self-reinforce. Demand drives issuance, issuance expands circulation, circulation supports more applications, and applications in turn create more demand. This forms a closed loop.

V. Structural Features: From Product to Network

Synthesizing the three layers of issuance, circulation, and application, the on-chain dollar network can be summarized as a three-layer structure:

First layer: Issuance nodes responsible for minting and redemption, controlling supply boundaries.

Second layer: Settlement network responsible for transfer and accounting, forming value flow channels.

Third layer: Financial protocols responsible for interest rate generation and risk pricing, building credit expansion mechanisms.

These three layers form a structural closed loop.

Compared to the traditional dollar system, the difference lies not in monetary essence but in operational mechanism:

Settlement relies on blockchain ledgers;

Accounts are replaced by wallet addresses;

Interest rates are partly generated by protocol algorithms;

Cross-border transfers do not require bank intermediaries.

This is a “technology-driven dollar distribution network,” not a new sovereign currency system. Stablecoins have not created a new monetary entity but have changed the organizational model of the dollar.

VI. Macroeconomic Implications: Extension and Redistribution of the Dollar Network

The expansion of the on-chain dollar network means increased channels for dollar circulation.

Anyone with an on-chain address can directly hold and transfer stablecoins without relying on traditional bank accounts.

This brings three macro-level effects:

First, lowers the threshold for dollar access.

Second, changes cross-border capital flow pathways.

Third, partially replaces financial intermediaries with technology.

However, it must be emphasized that the on-chain dollar network has not left the real regulatory environment. Fiat-backed stablecoins are still subject to legal and banking system influences; crypto-collateralized stablecoins are still constrained by market risks; on-chain financial activities still face compliance and audit challenges.

Therefore, it is an extension at the technological level rather than a replacement at the institutional level. Structurally, when the following three conditions occur simultaneously, a dollar subnet can be considered formed:

Stablecoins become major units of account;

Financial protocols build yield structures around stablecoins;

Cross-chain and cross-platform circulation forms sustained liquidity.

At this point, stablecoins are no longer merely transaction media but have become part of a complete dollar circulation network.

VII. Lesson Summary

The core conclusion of this lesson is: As stablecoins expand in scale and deepen in functionality, they gradually form an on-chain dollar network structure.

Its foundation is determined by issuance mechanisms;

Its operation is supported by circulation networks;

Its expansion is reinforced by financial protocols;

Its stability is constrained by reserves and risk parameters.

The significance of stablecoins thus shifts—from settlement tools to becoming the liquidity core of on-chain financial systems.

In the next lesson, we will further discuss how on-chain credit is generated atop this network, and how lending and interest rate mechanisms form new risk pricing systems.

The network has already formed; its credit structure is just beginning.

Lesson 1:The Essence of Stablecoins—On-Chain Mapping of the US Dollar

Lesson 2:From Stablecoins to On-Chain Dollar Networks

Lesson 3:From Stablecoins to On-Chain Credit: The Formation of Interest Rates and Lending Structures

Lesson 4:On-Chain Finance vs. Traditional Finance: Structural Comparison and Boundary Redefinition

Lesson 5:The Institutional Evolution of Tokenized Assets and On-Chain Infrastructure

Related Courses

The Beginner's Guide to Blockchain-based Airdrops

Crypto Mining Equipment

Learn about web3 data and analytics

Identity in Crypto: Main Projects

Crypto Mining