The Essence of Stablecoins—On-Chain Mapping of the US Dollar

This chapter outlines the institutional origins and credit structure of stablecoins, explaining how they serve as on-chain representations of the US dollar and form the foundational layer for settlement and valuation in on-chain finance.

I. Starting Point: Why On-Chain Systems Need Stable Assets

In any financial system, a stable unit of account and an efficient settlement mechanism are structural prerequisites. Without a unified measure of value, prices cannot be expressed; without reliable settlement tools, transactions cannot be completed in full. While early crypto asset markets achieved the technical breakthrough of “decentralized bookkeeping,” they long lacked a stable value anchor and settlement layer.

Native assets like Bitcoin and Ethereum offer scarcity and verifiability, but their high price volatility makes them unsuitable as stable units of account. At the same time, the traditional banking system cannot be directly integrated into blockchain networks; fiat money inflows and outflows rely on exchanges and bank accounts, making settlement paths complex and limiting efficiency. In this context, on-chain markets have the ability to issue and transfer assets but lack a complete financial structure.

The emergence of stablecoins addresses this structural gap. They are not designed merely for “price stability,” but to establish a sustainable settlement foundation within blockchain environments. The core issue is not volatility, but the reconstruction of credit and settlement mechanisms.

II. Institutional Design: How the US Dollar Is Mapped On-Chain

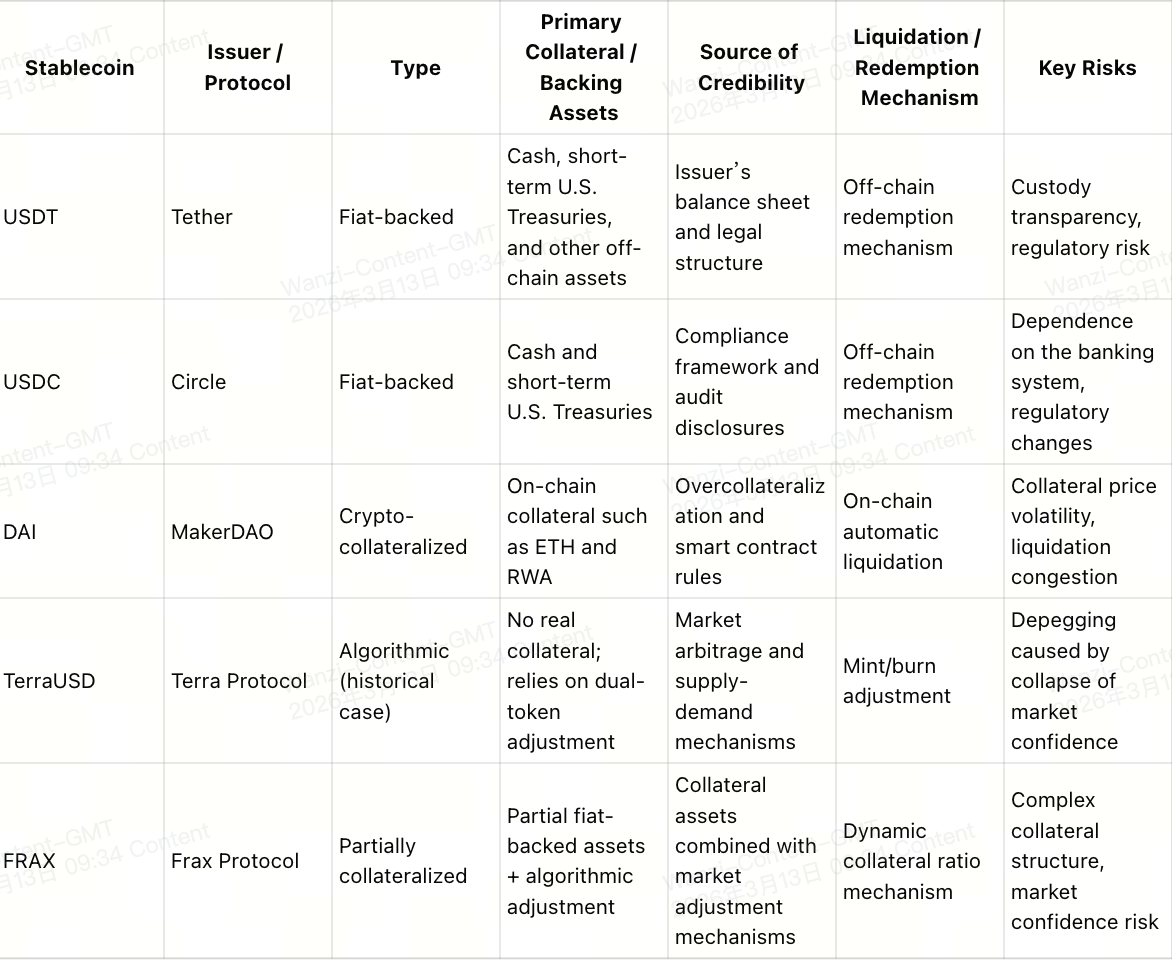

Currently, mainstream stablecoins are built on a fiat reserve model. Notable examples include USDT issued by Tether and USDC issued by Circle. The basic logic is straightforward: issuing institutions hold US dollar cash or highly liquid assets off-chain and mint an equivalent number of tokens on-chain at a 1:1 ratio, promising redemption channels under specific conditions.

The key to this model lies not in technical complexity, but in credit structure arrangement. Stablecoin holders do not directly own US dollar deposits; instead, they hold digital claims on reserve assets. The blockchain records the token’s flow path, while the issuing institution manages reserve assets and redemption processes. On-chain transparency combined with off-chain custody creates a hybrid credit framework.

Structurally, fiat-reserved stablecoins have the following characteristics:

Clearly defined value anchor, reliant on real-world assets;

High liquidity, enabling large-scale settlement and cross-platform circulation;

Risk concentrated in the issuer’s compliance and asset management capabilities.

This design allows stablecoins to gain broad market acceptance in a short time and become the mainstream choice for trading pairs and settlement assets.

III. Functional Positioning: Settlement Layer, Not Investment Layer

It is inaccurate to view stablecoins as “low-volatility assets.” Their institutional role is more akin to settlement-layer assets in financial systems. Stablecoins themselves do not generate returns; their value derives from convertibility and liquidity rather than capital appreciation expectations.

In on-chain markets, stablecoins fulfill three basic functions:

Unit of account: Most token prices are denominated in stablecoins, creating a unified pricing framework;

Settlement medium: Transfers between different trading platforms and chains are primarily conducted through stablecoins;

Risk buffer tool: When market risk rises, funds can quickly move into stablecoins to reduce exposure to asset volatility.

These functions collectively form the foundation of on-chain finance. Without stablecoins, trading would revert to direct swaps between highly volatile assets, making price systems unstable and hindering the formation of derivatives and lending markets.

Therefore, the value of stablecoins does not lie in “upside potential,” but in “system stability.” They are more akin to settlement currencies in financial infrastructure than investable risk assets.

IV. Model Differences: Institutional Paths with Different Sources of Credit

Beyond fiat-backed models, the market has explored other stabilization mechanisms. Crypto-collateralized stablecoins, represented by DAI issued by MakerDAO, generate stablecoins by overcollateralizing on-chain assets. Their operational logic relies on smart contracts for automated execution. When the collateralization ratio falls below a safety threshold, liquidation is triggered to maintain the overall solvency of the system.

The advantages of this model include:

Reduced dependence on a single centralized custody institution;

Transparent operating rules, with risk parameters that can be publicly adjusted.

However, its risks are also evident:

Sharp volatility in collateral asset prices may trigger cascading liquidations;

When liquidity is insufficient, liquidation efficiency may decline.

Another approach is the algorithmic stabilization mechanism, such as the dual-token model adopted by TerraUSD and LUNA. This structure adjusts supply and demand through mint-and-burn mechanisms, theoretically maintaining the peg. However, when market confidence declines and liquidity contracts, the algorithmic adjustment mechanism may fail, leading to depegging.

The core differences among these models lie in their sources of credibility:

Fiat-backed models rely on real-world assets and legal frameworks;

Crypto-collateralized models rely on on-chain assets and automated liquidation logic;

Algorithmic models rely on market expectations and arbitrage mechanisms.

Ultimately, the sustainability of a stabilization mechanism depends on the strength of its credit backing and its liquidation capacity, rather than the complexity of its design.

V. Structural Impact: Changes in US Dollar Circulation Paths

Stablecoins have not changed the sovereign status of the US dollar but have altered its circulation method. In traditional finance, US dollar transfers rely on bank accounts and settlement networks; in on-chain systems, wallet addresses and blockchain ledgers serve as the foundation. Stablecoins enable holding and transferring US dollar value without traditional bank accounts.

This change brings several structural impacts:

Settlement time shifts from business hours to 24/7 continuous operation;

Cross-border transfers no longer depend on traditional payment systems;

Funds can move quickly between different chains and platforms.

From a macro perspective, stablecoins lower the threshold for using US dollars and allow liquidity to break through the limitations of bank account systems. This process is not currency substitution but a technological upgrade in distribution.

VI. Foundational Role: Prerequisite for On-Chain Credit Systems

On-chain lending protocols, derivatives markets, and liquidity pools all use stablecoins as core units of account. Interest rate formation requires a stable principal benchmark; margin systems need relatively low-volatility collateral assets. Stablecoins thus form the starting point for on-chain credit expansion.

Without stablecoins, on-chain financial activities would revolve around highly volatile assets, making it difficult to establish predictable yield structures or risk management frameworks. What stablecoins provide is not a growth logic but a stability logic—the basis for building interest rate markets and risk pricing mechanisms.

In this sense, stablecoins can be viewed as the “monetary layer” within on-chain systems. Their presence transforms blockchains from mere asset issuance and transfer networks into systems that gradually acquire financial functionality.

VII. Lesson Summary

This lesson establishes three core understandings:

Stablecoins are not speculative tools but settlement tools;

Stablecoins are not new currencies but digital representations of the US dollar;

Stablecoins are not single products but credit and settlement structures embedded within blockchain systems.

The institutional significance of stablecoins lies in providing unified units of account and settlement layers for on-chain systems, making subsequent lending, derivatives, and asset management activities possible. Understanding this foundational structure is essential for analyzing on-chain financial systems.

The next lesson will further discuss how stablecoins evolve from simple settlement tools into an “on-chain US dollar network” spanning issuance, circulation, and application layers—and how they become the core source of liquidity for on-chain financial infrastructure.

Lesson 1:The Essence of Stablecoins—On-Chain Mapping of the US Dollar

Lesson 2:From Stablecoins to On-Chain Dollar Networks

Lesson 3:From Stablecoins to On-Chain Credit: The Formation of Interest Rates and Lending Structures

Lesson 4:On-Chain Finance vs. Traditional Finance: Structural Comparison and Boundary Redefinition

Lesson 5:The Institutional Evolution of Tokenized Assets and On-Chain Infrastructure

Related Courses

The Beginner's Guide to Blockchain-based Airdrops

Crypto Mining Equipment

Learn about web3 data and analytics

Identity in Crypto: Main Projects

Crypto Mining