Mechanism Comparison of Leading DeFi Lending Protocols: Aave, Morpho and Maple

This lesson will take three representative protocols—Aave, Morpho and Maple as core samples. From three dimensions: liquidity pool structure, interest rate formation mechanism, and risk management logic, it systematically dissects how DeFi lending has gradually evolved from a "unified market" to a "stratified financial system".

I. Aave: An Infrastructure Model with Unified Liquidity Pools

Image: https://app.aave.com/

Among all DeFi lending protocols, Aave is the most typical one that is closest to the form of financial infrastructure. It does not pursue extreme efficiency or customization, but prioritizes solving three problems: accessibility, predictability, and system stability.

1. Unified Liquidity Pools: A Universal Market Design

Aave’s core design is Pooled Liquidity:

- All depositors inject the same type of assets into a single liquidity pool

- All borrowers take out assets from this pool

- Interest rates are automatically adjusted based on overall supply and demand

This structure is essentially a “shared risk, shared liquidity” design, with distinct advantages:

- Highly concentrated liquidity that is not prone to fragmentation

- Permissionless entry for participants at any capital scale

- Highly predictable user behavior and protocol outcomes

For both the early and current stages of DeFi, this universal market design has greatly lowered the barriers to understanding and usage, making Aave the default underlying lending module for numerous protocols, strategies, and institutions.

2. Interest Rate Model: A Single Curve Driven by Utilization Rate

Aave’s interest rate mechanism is based on one core metric:

Utilization Rate = Borrowed Funds / Total Deposited Funds

- When the utilization rate rises, indicating tight liquidity, borrowing interest rates go up;

- When the utilization rate falls, indicating ample liquidity, interest rates decline.

The advantages of this single-curve model are:

- Clear logic for interest rate changes

- Intuitive market signals

- No reliance on complex parameters or subjective judgments

However, its trade-offs are equally obvious: All borrowers bear the “average risk pricing”. High-quality collateral and marginal-risk borrowing are not effectively differentiated in terms of interest rates. This is a plus for security but a minus for capital efficiency.

3. Risk Management Logic: Parametric, Not Personalized

Aave’s risk control relies heavily on a standardized parameter system:

- Loan-to-Value (LTV) Ratio

- Liquidation Threshold

- Liquidation Penalty

These parameters are set at the asset level, not the user or strategy level. This means:

- Extremely strong overall security of the protocol

- High scalability and replicability

- Inability to finely distinguish between risk and capital efficiency

From a financial perspective, Aave is more like the On-chain Money Market of the DeFi world: stable, transparent, and shock-resistant, yet not pursuing extreme efficiency.

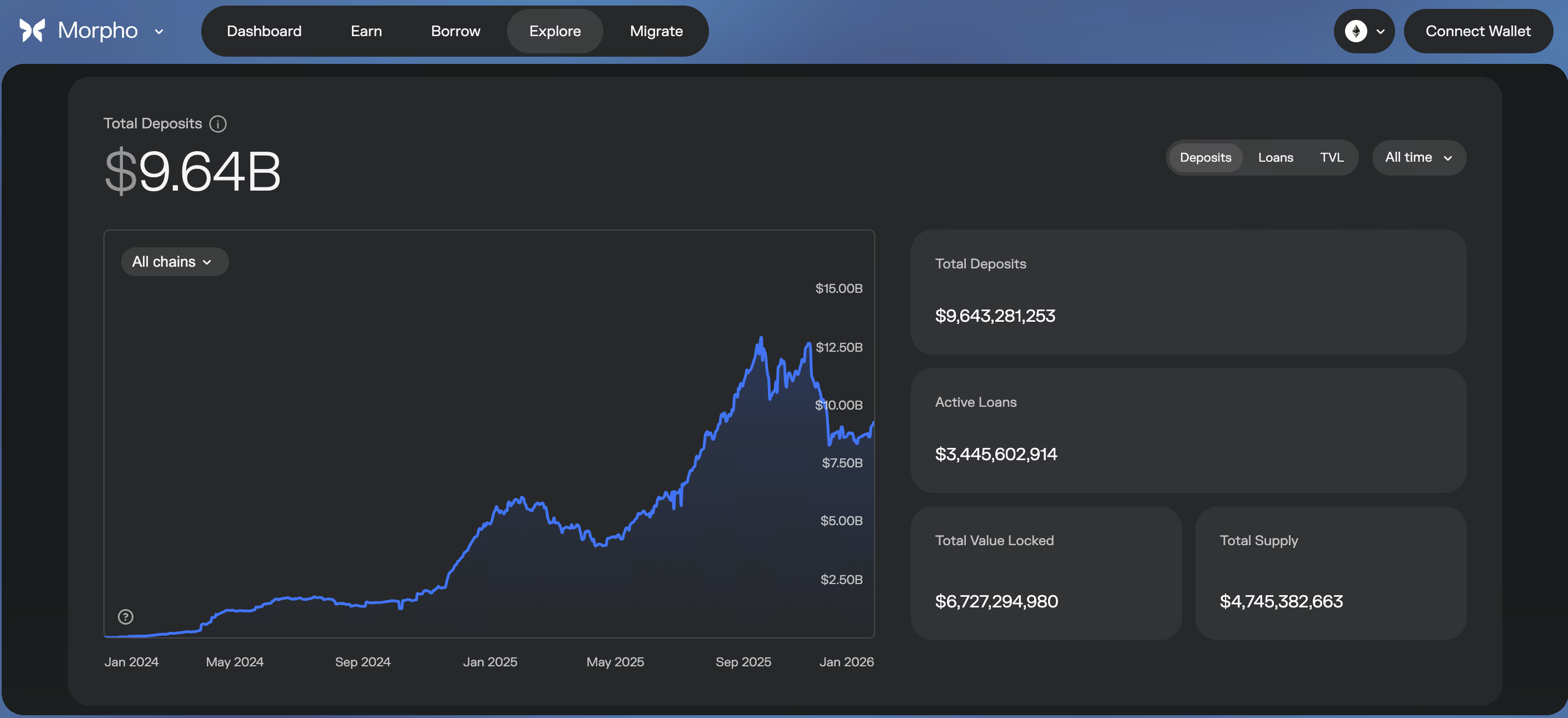

II. Morpho: Restructuring the “Efficiency Layer” on Top of Unified Pools

Source: https://app.morpho.org/ethereum/explore

If Aave solves the question of “whether the market exists”then Morpho solves the question of “whether the market is efficient enough”.

1. A Stacked Model with Point-to-point Matching

Morpho does not overthrow Aave’s infrastructure; instead, it chooses to stack on top of it:

- Depositors and borrowers are prioritized for the point-to-point matching

- Unmatched portions are automatically routed back to the Aave pool

This design brings three key changes:

- Lenders earn higher returns

- Borrowers pay lower interest rates

- The overall liquidation and risk of the protocol are still borne by Aave

Morpho is not essentially an independent lending market, but rather an efficiency layer built on top of Aave.

2. Interest Rates Are No Longer a “Single Curve”

In Morpho, the logic of interest rate formation has changed:

- P2P lending interest rates fall between Aave’s deposit rate and borrowing rate

- The actual interest rate is determined by matching efficiency and the structure of supply and demand.

This enables interest rates to have:

- Stronger competitiveness

- Finer price discovery

- A pricing mechanism that is closer to real supply and demand

To a certain extent, Morpho transforms Aave’s “passive algorithmic pricing” into “active matching-based pricing”.

3. Restrained Redistribution of Risk

Morpho does not introduce new liquidation or credit models; instead:

- Credit and systemic risks remain anchored to Aave

- Credit and systemic risks remain anchored to Aave

This is an extremely conservative yet ingenious design: it does not create new risks, but only redistributes efficiency.

Precisely because of this, Morpho is highly attractive to conservative capital, institutional strategies, and long-term funds.

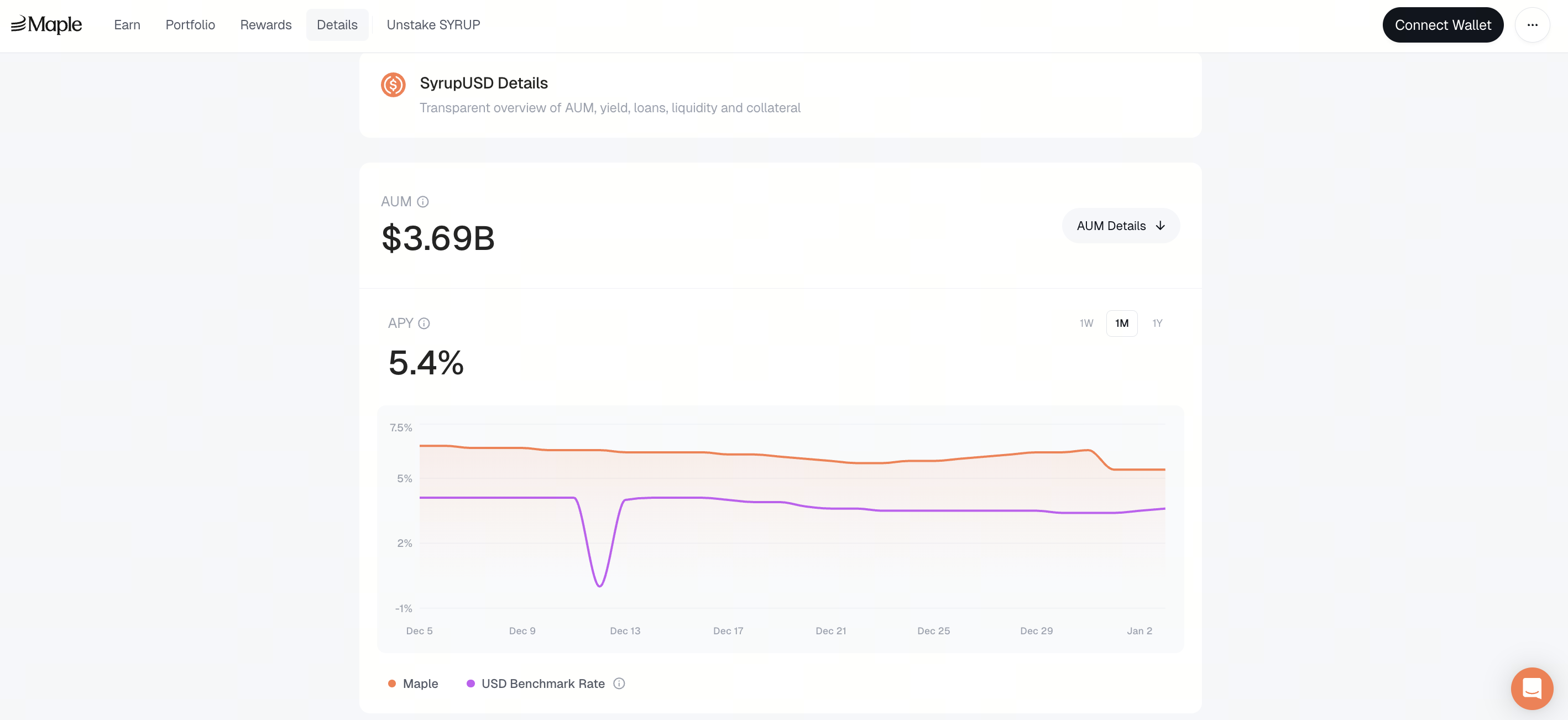

III. Maple: A Credit Lending Model for Institutions

Source: https://app.maple.finance/earn/details

If Aave and Morpho still belong to the “over-collateralization logic”, then Maple represents the credit-oriented attempt in DeFi lending.

1. Pools as Strategies, Not Public Markets

Maple’s core is not a unified market, but the concept of “Pools as Strategies”.

- Each lending pool has independent rules

- Clearly defined borrowers and capital usage purposes

- Explicit interest rates, tenors, and risk expectations

This makes Maple more akin to:

- Private credit

- Structured finance

- On-chain debt markets

It does not attempt to serve all users, but rather serves assessable borrowing entities.

2. Interest Rates Determined by Risk Assessment, Not Algorithms

In Maple:

- Interest rates are not automatically generated by utilization curves

- Instead, they are jointly determined by the borrower’s creditworthiness, tenor structure, and market conditions

The outcomes of this are:

- More stable interest rates

- More predictable returns

- A noticeable reduction in transparency and decentralization

This is a clear trade-off that Maple has made to enhance institutional usability.

3. Fundamental Changes in Risk-Bearing Methods

Maple’s risk control does not rely on real-time liquidation, but on:

- Risk control and supervision by Pool Delegates

- Legal agreement constraints

- Governance and accountability mechanisms

This marks a new stage in DeFi lending: risks are no longer fully resolved by code, but are jointly borne by institutions and contracts.

IV. Essential Differences Between the Three Models

From a higher-dimensional perspective, these three protocols are not in direct competition, but rather have functional divisions of labor:

- Aave: Unified, open, and risk-resistant

- Morpho: Efficiency enhancement and interest rate optimization

- Maple: Credit-stratified and institutionally customized

They do not represent a hierarchy of “which is more advanced”, but rather cater to:

- Different risk appetites

- Different capital attributes

- Different financial use cases

V. DeFi Lending Is Moving Toward “Structural Stratification”

A clear trend is emerging: DeFi lending is evolving from a “single market” to a “multi-layered market system”.

- Bottom Layer: High-security, low-efficiency unified liquidity pools

- Middle Layer: Efficiency enhancement and matching mechanisms

- Top Layer: Institutional markets with differentiated credit, tenors, and usage purposes

This is not accidental, but an on-chain replication of the decades-long evolution path of traditional finance.

Lesson 1:Why DeFi Lending Is Becoming Financial-Grade Infrastructure

Lesson 2:Mechanism Comparison of Leading DeFi Lending Protocols: Aave, Morpho and Maple

Lesson 3:Interest Rate Models, Liquidation Mechanisms, and Systemic Risks in DeFi Lending

Lesson 4:How Institutions Use DeFi Lending: Stablecoins, Leverage, and On-Chain Arbitrage

Lesson 5:The Next Phase of DeFi Lending: Credit, RWAs, and Structural Integration with Off-Chain Finance

Related Courses

The Beginner's Guide to Blockchain-based Airdrops

DeFi Fundamentals

Crypto Mining Equipment

Identity in Crypto: Main Projects

Learn about web3 data and analytics