Interest Rate Models, Liquidation Mechanisms, and Systemic Risks in DeFi Lending

This lesson systematically analyzes the interest rate models and liquidation mechanisms in DeFi lending, explains how they regulate risks and maintain system stability, and examines the systemic risks faced by lending protocols under extreme market conditions and their response strategies.

I. Interest Rates Are Not Yield Tools, But Risk Regulators

In the DeFi lending system, the primary function of interest rates is not to “provide a return on capital” but to regulate the speed, direction and magnitude of systemic risk exposure.

In other words, interest rates are essentially a risk regulator, not a marketing tool.

A healthy lending protocol’s interest rate mechanism must at least fulfill three purposes simultaneously:

- Curb excessive borrowing and prevent the system from continuously accumulating risks in a single direction

- Attract or release liquidity, guiding the reallocation of capital when supply and demand are imbalanced

- Send signals before pressure actually arrives, allowing the market to react ahead of liquidations

This is why nearly all mainstream DeFi lending protocols adopt a dynamic interest rate model rather than fixed rates. In the on-chain environment, interest rates are not a “price”, but a real-time indicator of system health.

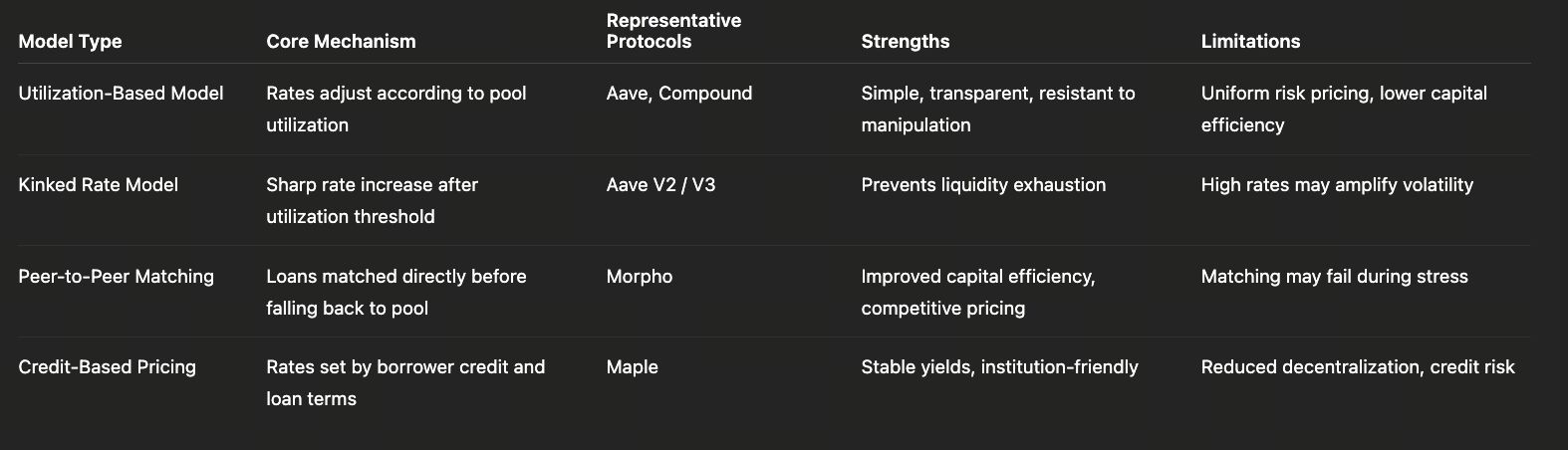

II. Three Paradigms of Mainstream Interest Rate Models

1. Utilization-Driven Model (Aave/Compound)

This is the most classic and widely applied interest rate model in DeFi, with only one core variable: Utilization Rate = Borrowed Funds / Total Deposited Funds

Its basic logic is straightforward:

- Low utilization rate → Ample liquidity → Low borrowing interest rates

- High utilization rate → Tight liquidity → Sharply rising interest rates

To prevent the system from spiraling out of control in the high-utilization range, protocols usually set a kink (inflection point):

- Before the kink: Interest rates rise slowly, encouraging normal borrowing activity

- After the kink: Interest rates surge sharply, forcibly curbing new borrowing demand

Advantages

- Simple and transparent model

- Clear market signals

- Strong resistance to manipulation

- Highly scalable and replicable

Limitations

- All borrowers bear the same risk premium

- Unable to distinguish between “healthy leverage” and “high-risk leverage”

- Low capital efficiency under complex strategies

Therefore, this type of model is more suitable as an infrastructure-layer interest rate mechanism rather than a refined risk pricing tool.

2. Point-to-point / Semi-Marketized Interest Rate Model (Morpho)

The key change introduced by Morpho is that interest rates are no longer determined entirely by “pool status”, but by supply-demand matching efficiency.

In Morpho, when P2P matching is successful:

- Borrower pays costs lower than the pool borrowing rate

- Lenders earn a higher return than the pool deposit rate

This essentially introduces a micro-level competitive pricing mechanism on top of unified pools.

Advantages

- Significant improvement in capital efficiency

- More granular interest rate signals

- Emergence of “multi-tier interest rate ranges” for the same asset

Potential Risks

- Matching may fail rapidly under extreme market conditions

- The system remains highly dependent on the underlying pool as a liquidity and liquidation buffer

Thus, Morpho’s success is premised on one condition: the underlying pool itself must be sufficiently robust, predictable, and shock-resistant.

It does not replace infrastructure, but rather builds an efficiency enhancement layer on top of it.

3. Credit and Manual Pricing Model (Maple)

In Maple, the interest rate logic has undergone a fundamental change:

Interest rates are no longer automatically generated by algorithms, but are jointly determined by the following factors:

- Borrower’s credit quality

- Loan term structure

- Market conditions and risk appetite

This makes it closer to the credit spread pricing model in traditional finance.

Advantages

- Low interest rate volatility

- Highly predictable returns

- More suitable for institutional liability management and asset allocation

Trade-offs

- Noticeable decline in decentralization

- Systemic risks shift from “market risks” to “credit and legal risks”

This is a clear trade-off that Maple has made to enhance institutional usability and controllability.

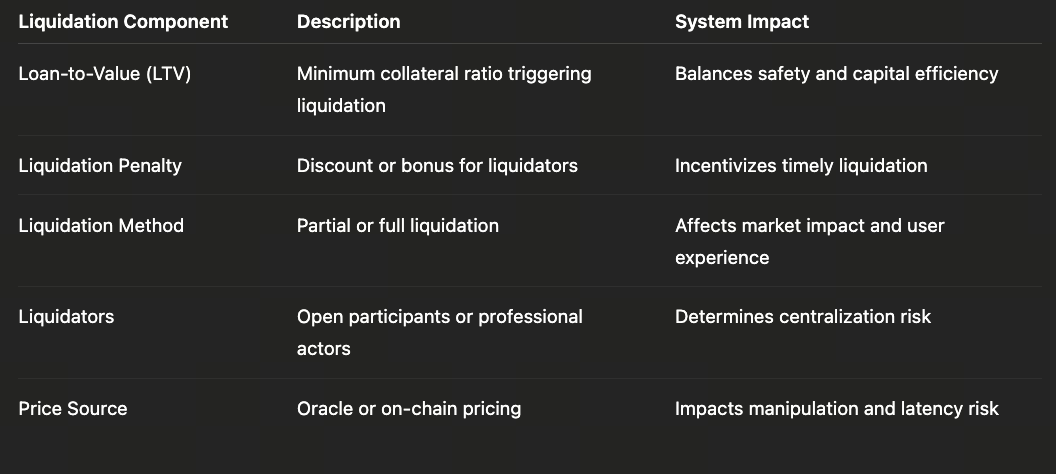

III. Liquidation Mechanism: The True “Insurance System” of DeFi Lending

If interest rates are responsible for pre-emptive risk adjustment, then the liquidation mechanism is in charge of in-loss mitigation. In DeFi lending, liquidation is not an abnormal event, but an integral part of the system design.

1. Basic Logic of Automated Liquidation

In over-collateralized lending, the liquidation process typically unfolds as follows:

- Collateral asset prices decline

- Loan-to-Value ratio falls below the liquidation threshold

- The system allows third parties to perform forced liquidation

Liquidators are rewarded with:

- The right to purchase collateral assets at a discount

- Compensation for assuming price volatility risks

This mechanism relies on a core assumption: that there’s always market liquidity willing to step in.

2. Three Key Design Variables in Liquidation Mechanisms

(1) Liquidation Threshold

- Higher threshold → Greater system security, but lower capital efficiency

- Lower threshold → The higher the capital efficiency, but the greater the tail risk

(2) Liquidation Penalty

- Excessively low penalty → Insufficient incentive for liquidators to participate

- Excessively high penalty → Excessive costs for borrowers, dampening lending demand

(3) Liquidation Method

- Partial liquidation vs. Full liquidation

- Dutch auction vs. Immediate execution

These parameters are interdependent and together determine system resilience during extreme volatility.

IV. What Happens When Markets Fail?

The theoretically sound liquidation mechanism does not always hold up under extreme market conditions.

DeFi’s history has repeatedly proven that:

- A decline in price does not guarantee available liquidity

- On-chain congestion amplifies liquidation delays

- Collateral asset correlation surges sharply under market stress

When these scenarios occur simultaneously, the system faces not just individual risks, but systemic risk.

V. Three Typical Sources of Systemic Risk

1. High Correlation of Collateral Assets

When lending is heavily concentrated in similar collateral types:

- ETH, LST, and LRT prices drop concurrently

- Liquidations are triggered en masse

- Market liquidity is drained instantaneously

2. Oracle And Price Lags

- Delayed price updates

- Manipulation of low-liquidity markets

- Mismatches between off-chain prices and on-chain settlements

All of these directly undermine the effectiveness of liquidation mechanisms.

3. Centralization of Liquidators

In reality:

- Liquidation relies heavily on a small number of specialized teams

- Success depends largely on MEV advantages and robust infrastructure

This means liquidation itself carries centralization risks.

VI. How Protocols Address Systemic Risk

Mature lending protocols have begun to implement multi-layered defense mechanisms:

- Dynamic adjustment of risk parameters

- Supply/Borrow Caps

- Insurance funds and bad debt buffers

- Governance intervention in extreme cases

These mechanisms mark a crucial shift: DeFi lending is evolving from a “fully automated system” to a “governable financial system”.

VII. Summary

The true competitiveness of DeFi lending does not lie in:

- Offering higher interest rates

- Providing greater leverage

But in:

- Sustained operation under market stress

- Timely and transparent exposure of risks

- Built-in self-healing capabilities of the system

When the market starts focusing on these aspects, DeFi is no longer just an experiment, but assuming the role of financial infrastructure.

Lesson 1:Why DeFi Lending Is Becoming Financial-Grade Infrastructure

Lesson 2:Mechanism Comparison of Leading DeFi Lending Protocols: Aave, Morpho and Maple

Lesson 3:Interest Rate Models, Liquidation Mechanisms, and Systemic Risks in DeFi Lending

Lesson 4:How Institutions Use DeFi Lending: Stablecoins, Leverage, and On-Chain Arbitrage

Lesson 5:The Next Phase of DeFi Lending: Credit, RWAs, and Structural Integration with Off-Chain Finance

Related Courses

The Beginner's Guide to Blockchain-based Airdrops

DeFi Fundamentals

Crypto Mining Equipment

Identity in Crypto: Main Projects

Learn about web3 data and analytics