What Is TradFi (Traditional Finance)? A Complete Guide

In the current global financial landscape, TradFi manages hundreds of trillions of dollars in assets across markets including stocks, bonds, forex, commodities, and derivatives. By leveraging regulated intermediaries, this model facilitates saving, lending, investing, payments, and risk management—serving as the core engine of the modern economic system.

As blockchain and Decentralized Finance (DeFi) mature, TradFi is undergoing a systemic upgrade through tokenization, on-chain settlement, and hybrid finance models. Establishing a systematic understanding of TradFi—including its definition, how it works, TradFi accounts, core asset types, the key differences between TradFi and DeFi, and evolutionary trends—is essential to grasping its role as the bedrock of the modern economy.

What Is TradFi (Traditional Finance)? A Complete Guide

What is TradFi?

TradFi, short for Traditional Finance, is the established financial framework that most people globally rely on daily. Its core origins trace back to medieval banking, evolving over centuries into a trust mechanism centered on sovereign credit and centralized institutions.

Under the management system of traditional financial accounts, users can access stock markets with a total market capitalization exceeding $100 trillion, along with various safe-haven assets. This system operates under the supervision of central banks, the Federal Reserve, or the Securities and Exchange Commission (SEC) to ensure market fairness and consumer protection.

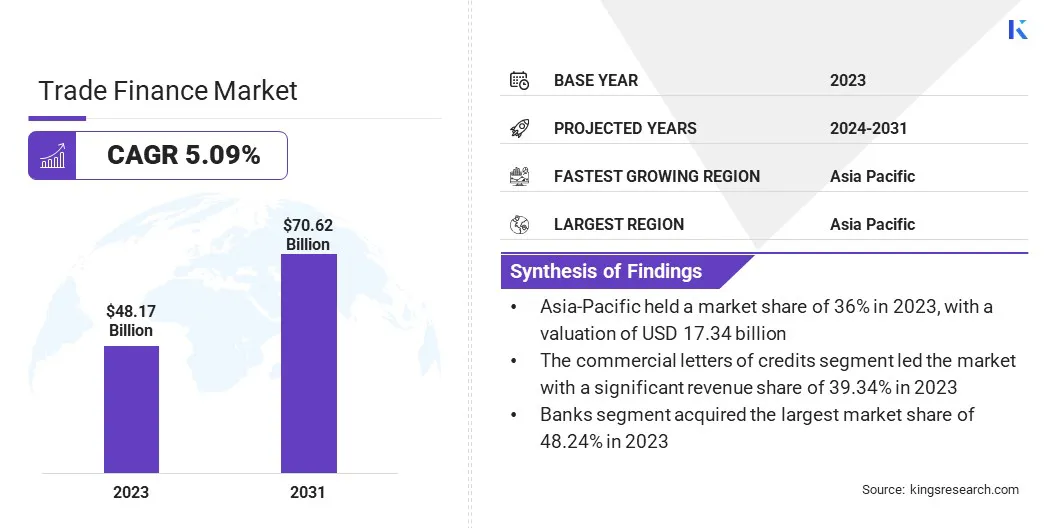

TradFi remains the foundation of the modern economy. According to Kings Research, the global trade finance market size was 48.17billionin2023andisprojectedtoreach48.17 billion in 2023 and is projected to reach 48.17billionin2023andisprojectedtoreach70.62 billion by 2031.

tradfi-marketcap

As the liquidity backbone of the global economy, TradFi supports corporate financing and personal consumption through deposit and loan mechanisms, driving GDP growth. Capital markets connect savers and investors, facilitating infrastructure, trade, and employment. Without TradFi, critical services like cross-border payments, mortgages, and insurance would cease to function, directly impacting the lives of billions.

How Does TradFi Work?

The robust operation of TradFi relies on a matrix of institutions with clearly defined functions. Central banks, commercial and retail banks, investment banks, brokers, and regulators work together to ensure the transmission of monetary policy and the expansion of the credit system.

The operational mechanism of TradFi follows standardized processes for capital raising, risk assessment, trade matching, and clearing/settlement:

-

Capital Allocation: Banks gain liquidity by accepting deposits and transforming them into loans for borrowers, profiting from the interest rate spread.

-

Clearing and Settlement: Transactions are verified by centralized networks (such as SWIFT), typically requiring a settlement lag of 1 to 3 business days.

-

Regulation and Stability: Regulators set rules and monitor compliance to mitigate systemic risks caused by single points of failure.

In short, the TradFi process usually begins with a user deposit. The bank manages credit risk while lending those funds to borrowers. For trading, transactions are matched on an exchange, executed by brokers, and settled by clearinghouses within a T+1 or T+2 timeframe. Central banks maintain stability via interest rate policies and open market operations, while insurance companies and derivative markets hedge against fluctuations in exchange rates and market volatility.

Key Components of TradFi

A complete TradFi ecosystem consists of several collaborative pillars, each responsible for different financial functions:

Key Participants

Banks, including retail and investment banks, sit at the center of TradFi. They provide deposit services, lending, and payment settlement, acting as the main conduit for capital flows. Capital markets and stock exchanges enable the trading of equities and bonds, helping companies raise funds while allowing investors to diversify risk. Insurance companies manage uncertainty by transferring risk through policies that protect individuals and businesses.

Financial Market Infrastructure

Financial markets form another core component of TradFi, encompassing money markets for short-term liquidity, capital markets for long-term financing, foreign exchange markets, and derivatives markets. These systems allocate resources across time and geography, supporting trade and hedging activities. Payment processors and clearing systems, such as the SWIFT network, ensure efficient global transaction settlement.

Regulation and System Stability

Regulatory bodies, including central banks and securities regulators, establish rules to ensure fairness, stability, and consumer protection. Core banking systems and IT infrastructure support account management, transaction processing, and financial reporting across the entire ecosystem.

Key Characteristics of TradFi

TradFi is characterized by centralized control, strict regulation, identity-based trust, and specific settlement cycles. While this structure emphasizes stability, it can sometimes limit efficiency.

Centralization

In TradFi, all transactions and decisions revolve around centralized institutions (such as banks, central banks, and stock exchanges). These entities act as “anchors of trust,” responsible for record-keeping, clearing, and maintaining market order.

This also implies that users do not have absolute “ownership” of their accounts, as institutions reserve the right to freeze assets or restrict transactions.

Intermediation & Regulation

TradFi is an ecosystem composed of multiple layers of intermediaries. Whether opening an account or transferring funds, users must pass KYC (Know Your Customer) and AML (Anti-Money Laundering) screenings. Furthermore, brokers, custodians, clearinghouses, and insurers act as the “lubricants” of transactions, though their involvement leads to accumulated fees at every stage.

Identity-based Trust

In traditional finance, a user’s “creditworthiness” depends on identifiable information (social reputation, proof of income, residency, etc.). Consequently, financial services are typically opaque; banks determine loan eligibility and interest rates based on an individual’s specific background and identity.

Settlement Lag

Despite high levels of digitalization, the underlying logic of TradFi remains constrained by “business hours” and “clearing cycles.” For instance, stock trades or cross-border remittances often require 1 to 3 business days to achieve final settlement, as multiple institutions must perform back-end reconciliation.

High Barriers to Entry

Due to compliance costs and geographical limitations, TradFi is not accessible to everyone. Hundreds of millions of people globally remain “unbanked”—unable to access basic financial services because they lack official identification or live in remote regions.

What Types of TradFi Assets Are Moving On-Chain?

TradFi asset classes are undergoing a profound digital transformation. By 2026, on-chain traditional finance has expanded beyond early tokenized bonds into stocks, commodities, and derivatives.

TradFi ETFs

Exchange-Traded Funds (ETFs) are low-cost, basket-based investment instruments widely used across equities, bonds, commodities, and increasingly, crypto-related markets.

As the relationship between crypto and traditional finance deepens, products such as spot Bitcoin ETFs have become a key bridge between the two systems. These ETFs allow investors to gain crypto exposure through familiar TradFi structures, bringing institutional capital and liquidity into digital asset markets while maintaining regulatory alignment.

On-chain and crypto-linked ETF products further extend this access by enabling more flexible settlement, continuous trading, and integration with broader crypto portfolios.

TradFi Bonds

Bonds are legal debt instruments that represent a lending relationship between issuers and investors, and they remain a core financing tool for governments and corporations.

Through Real World Asset (RWA) tokenization, traditional bonds such as government debt are being converted into digital tokens that settle on-chain. This transition improves settlement speed, transparency, and accessibility while preserving the underlying economic structure of fixed-income products.

Industry data shows that tokenized RWA markets have grown to several billion dollars in value, positioning on-chain bonds as one of the most important liquidity bridges between traditional fixed-income markets and the crypto ecosystem.

TradFi Stocks

Stocks, or equities, represent ownership claims on a company’s assets and earnings and are central to capital markets.

Through tokenization and contract-based mechanisms, investors can now gain on-chain price exposure to major publicly listed companies such as Tesla, Apple, or NVIDIA. Compared with traditional brokerage accounts, on-chain stock exposure supports 24/7 trading, fractional participation, and lower capital thresholds.

It is important to note that these products typically provide economic price exposure rather than full shareholder rights, such as voting. However, they significantly reduce access barriers for global investors seeking equity exposure.

Gold and Commodities

Commodities form the physical foundation of the global economy, encompassing energy, metals, and agricultural products that anchor financial systems to real production and supply chains.

By bringing assets such as gold and silver on-chain, traditionally complex and storage-heavy commodities can be transformed into divisible, instantly settled digital representations. This improves liquidity and enables commodities to be used as collateral within DeFi protocols, expanding their role beyond passive value storage.

For investors, this model offers more efficient access to commodity markets while preserving their function as inflation hedges and safe-haven assets.

TradFi Derivatives

Derivatives such as futures, options, and foreign exchange contracts are core instruments for risk management, hedging, and capital efficiency in traditional finance.

By 2026, tokenized and crypto-integrated derivatives markets have expanded rapidly. Many platforms now replicate traditional derivative logic through perpetual contracts, index products, and synthetic assets, enabling 24/7 trading and faster settlement without traditional brokerage infrastructure.

This approach lowers participation thresholds while maintaining familiar pricing and risk mechanics, allowing crypto-native traders to engage directly with traditional market movements.

Advantages and Limitations of TradFi

For investors and enterprises alike, understanding the core value and inherent bottlenecks of TradFi (Traditional Finance) is essential in navigating today’s evolving financial landscape.

The primary strength of TradFi lies in its established legal protections, credit systems, and regulatory frameworks built over centuries.

-

Mature Asset Safety Nets: Unlike the crypto world, which is often plagued by smart contract vulnerabilities, TradFi offers greater fault tolerance. For instance, if a bank faces insolvency, government-backed deposit insurance schemes (such as the FDIC) protect depositors’ funds.

-

User Error Correction (The Right to Recourse): In cases of credit card fraud or accidental transfers, centralized institutions provide customer support and risk management systems that allow users to appeal and reverse transactions—a feature currently difficult to achieve with blockchain technology.

-

Stringent Regulatory Compliance: Through KYC (Know Your Customer) and AML (Anti-Money Laundering) screenings, TradFi effectively prevents financial crimes. This stability, backed by sovereign credit, makes it the preferred choice for global large-scale transactions and the real economy.

Despite its robustness, the centralized architecture of TradFi introduces significant efficiency issues and high operational costs.

-

Inefficiency and Settlement Lags: The underlying logic of TradFi depends on multiple intermediaries, including brokers, clearinghouses, and custodian banks. This complex chain extends transaction cycles; even in a digital age, cross-border remittances can take several days to settle, with each intermediary layer extracting additional service fees.

-

Natural Financial Exclusion: Driven by high compliance costs and profit margins, traditional banks maintain high barriers to entry. Globally, over 1.4 billion people remain “unbanked.” Due to a lack of formal identification, credit history, or geographical proximity, they are excluded from essential financial services.

-

Centralized Risks and Opacity: TradFi operations often function as a “black box.” It is difficult for average users to monitor an institution’s internal risk exposure in real-time. This creates single points of failure; if a core institution fails or makes a catastrophic decision (as seen in the 2008 financial crisis), it can trigger severe systemic economic instability.

TradFi vs DeFi: Key Differences

With the rise of blockchain technology and cryptocurrencies, Decentralized Finance (DeFi) has emerged as a new financial paradigm. By comparing TradFi vs. DeFi, it becomes evident that the two systems differ significantly in terms of architecture, regulation, accessibility, and settlement speed.

The fundamental difference between these two financial systems lies in their core logic: TradFi relies on centralized credit backing and strict regulatory frameworks; while it sacrifices some speed and ease of access, it provides robust security guarantees. In contrast, DeFi achieves the “disintermediation” of finance through blockchain technology. While DeFi offers distinct advantages in operational efficiency, global accessibility, and automated cost reduction, it also faces challenges stemming from technical vulnerabilities and regulatory vacuums.

| Dimension | Traditional Finance (TradFi) | Decentralized Finance (DeFi) |

|---|---|---|

| Architecture | Highly centralized; relies on banks/exchanges | Decentralized; based on smart contracts |

| Regulation | Strict (e.g., SEC); strong consumer protection | Nascent; high innovation but higher risk |

| Access | Requires approval; high barriers | Permissionless; requires only a wallet |

| Speed | Slow (T+1/2); days for cross-border | Near real-time; 24/7 operation |

| Cost | High fees (intermediary spreads) | Low gas fees; automated cost reduction |

| Assets | Fiat, Stocks, Bonds | Cryptocurrencies, Tokens |

| Risk | Systemic stability; deposit insurance | Smart contract bugs; market volatility |

Despite these differences, TradFi’s centuries-long presence ensures it will remain dominant in scale and influence. At the same time, DeFi’s innovation helps address certain inefficiencies in TradFi. Together, they are shaping the future of global finance.

How to Access TradFi via Crypto Platforms

As the integration between crypto platforms and TradFi enters a new stage, users no longer need to frequently transfer funds between banks and exchanges to access and trade TradFi assets. Furthermore, an increasing number of cryptocurrency platforms are providing financial infrastructure services, such as crypto debit cards, through deep integration with traditional banking systems, simplifying the transition from Web3 to real-world spending.

Taking Gate TradFi as an example, uusers can directly use their existing cryptocurrency accounts to access TradFi assets—including stocks, forex, gold, commodities, and stock indices. This eliminates the need for fiat deposits, physical asset ownership, or managing multiple platforms, enabling a one-stop operation to participate in global TradFi assets through a single exchange account.

How TradFi is Evolving

Entering 2026, TradFi is undergoing a profound transformation. It is no longer the antithesis of DeFi; instead, it is evolving into an “On-Chain Finance” model by absorbing technologies such as blockchain, AI, and RWA (Real-World Asset) tokenization.

Under this wave, global asset management giants like BlackRock have launched Spot Bitcoin ETFs and are driving the migration of assets such as government bonds and real estate onto the blockchain. Meanwhile, financial infrastructure entities including SWIFT and the DTCC are exploring ways to connect existing capital market systems with multi-chain networks through blockchain middleware technology. Simultaneously, traditional financial derivatives are migrating on-chain in the form of synthetic assets, enhancing settlement efficiency while preserving their core hedging functions.

Final Thoughts

TradFi serves as the cornerstone of global finance, built upon centralized intermediaries and rigorous regulatory frameworks. It has supported centuries of economic activity through efficient resource allocation and robust consumer protection. Despite limitations such as high costs and settlement lags, its mature legal framework remains irreplaceable.

Looking ahead, TradFi and DeFi are entering a phase of convergence: TradFi is becoming increasingly “DeFi-ized” through the adoption of smart contracts, while DeFi is steadily moving toward regulatory compliance. The deep integration of these two systems is driving the global financial landscape toward a more open, transparent, and programmable future.

FAQs

What is TradFi (Traditional Finance) and how does it affect daily life?

TradFi refers to traditional finance systems built on banks, exchanges, and legal frameworks. It underpins savings, loans, mortgages, insurance, and securities trading. Without it, modern economic activity would not function.

What are TradFi’s main strengths and weaknesses?

Strengths include strong regulation, consumer protection, stability, and deep liquidity. Weaknesses include reliance on intermediaries, high fees, slow settlement, and limited access in some regions.

What are the core differences between TradFi and DeFi?

The core differences between TradFi and DeFi lie in custody models, regulatory oversight, settlement speed, accessibility, and risk exposure. TradFi relies on centralized intermediaries and compliance frameworks, while DeFi operates through smart contracts with user-controlled custody and near-instant settlement.

How can users invest in TradFi assets today?

Users can trade U.S. stocks, forex, and gold CFDs via Gate TradFi.

What is TradFi’s future outlook in 2026?

Key trends include RWA tokenization, hybrid finance models, and deeper TradFi–DeFi integration.

Related Articles

AI-Native Settlement Layers: How United Stables Is Building the Next Financial Rail

The ve(3,3) Flywheel Explained: How AERO Tokenomics Powers Aerodrome’s DeFi Economy

How Does PAXG Work? In-Depth Overview of the Physical Gold Tokenization Mechanism

Aerodrome Tokenomics: How ve(3,3) Powers Base's Most Profitable DEX

How is the price of PAXG determined? Pegging mechanism, trading depth, and influencing factors