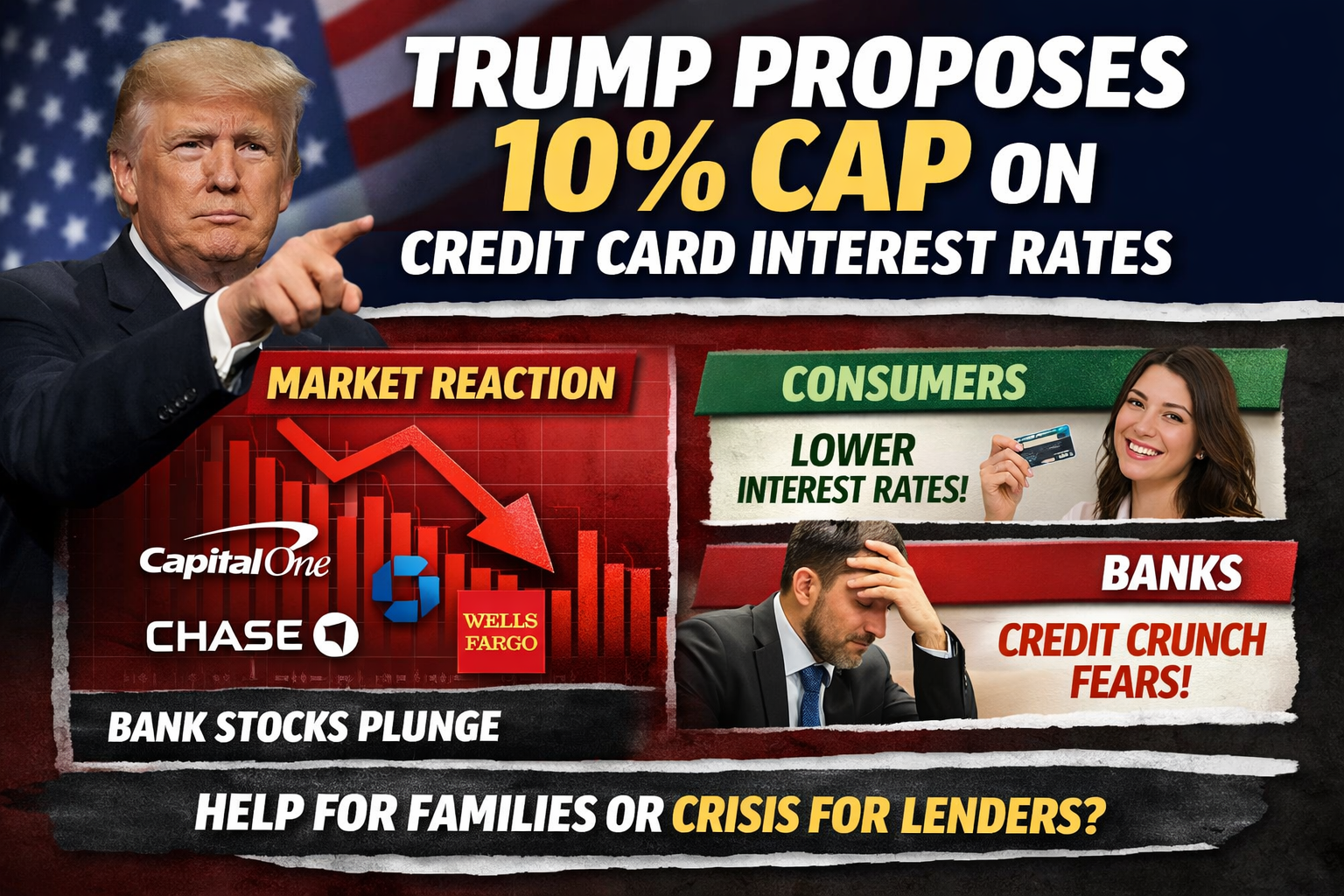

Trump Warns Credit Card Companies: Plans to Impose a 10% Interest Rate Cap After Taking Office, Triggering Market Turmoil

Trump’s Latest Policy Direction: Context of the Proposed 10% Credit Card Rate Cap

US President Donald Trump has recently reaffirmed on social media and in public statements that he plans to formally implement a one-year temporary cap on credit card interest rates, setting the annual maximum at 10%. Trump emphasized that current credit card rates have persistently remained in the 20%–30% range, or even higher, posing an unfair burden for ordinary consumers. He stated that if credit card companies fail to comply, such actions would be deemed “illegal.”

This initiative is being proposed against the backdrop of ongoing inflationary pressures and rising household debt costs. The intent is to ease the strain of high-interest debt on consumer cash flow, while also supporting his 2024 campaign commitment to reinforce the policy narrative of “lowering the cost of living.”

Policy Impact: Immediate Reaction from Bank Stocks and the Credit Card Sector

Following the policy announcement, financial markets responded swiftly. Financial institutions with significant credit card operations saw their stock prices come under pressure, with Capital One and Synchrony Financial experiencing notable declines. Major banks such as JPMorgan Chase and Citigroup also recorded substantial pullbacks.

Investors are primarily concerned about:

- Mandatory narrowing of credit spreads, threatening the high-profit model of credit card businesses;

- Potential disruption to banks’ overall profitability structures, especially those dependent on consumer finance;

- Pressure on financial sector valuations and increased short-term volatility.

Because high credit card rates have long been a major profit driver for banks, a steep reduction would force a rebalancing of profitability and capital allocation strategies.

Contrasting Positions: Consumer Support vs. Industry Opposition

From the consumer standpoint, the policy has won support from certain groups. For families struggling with high-interest credit card debt, the rate cap is viewed as a direct and tangible relief.

In contrast, financial institutions and industry groups have voiced clear opposition, citing several reasons:

- Potential tightening of credit supply: Lower rate caps reduce risk compensation, which may exclude borrowers with weaker credit histories;

- Cost shifting: Banks may compensate by raising annual fees, reducing cashback and rewards, or tightening card issuance standards;

- Shadow credit risks: Some consumers may be forced to turn to more expensive, less regulated alternative lending channels.

Organizations such as the Consumer Bankers Association have noted that while the goal is greater affordability, an excessively low mandatory cap could result in outcomes contrary to the original intent.

Legal and Regulatory Constraints: Significant Implementation Challenges

From an institutional standpoint, the president cannot unilaterally impose a nationwide rate cap through executive order. Such measures require legislation by the US Congress to have legal force.

Although proposals to limit credit card rates have been introduced in Congress:

- The legislative process is lengthy and marked by political divisions;

- The financial industry wields strong lobbying influence;

- There is considerable debate about potential side effects on the economy and credit system.

As a result, the market generally views the likelihood of this policy being enacted in the short term as limited.

Market Outlook and Summary

Overall, the 10% credit card rate cap is best seen as a policy proposal with strong political signaling. Its immediate effects are primarily reflected in market sentiment and stock price volatility, rather than in institutional changes.

- For investors, it’s important to monitor subsequent legislative developments, bank earnings, and shifts in credit data;

- For consumers, understanding the implications can help inform more rational decisions regarding interest rates, annual fees, and credit access.

If the policy moves forward, the US credit card and consumer finance industry could undergo a structural transformation, with impacts extending well beyond the rate itself.

Related Articles

AI-Native Settlement Layers: How United Stables Is Building the Next Financial Rail

The ve(3,3) Flywheel Explained: How AERO Tokenomics Powers Aerodrome’s DeFi Economy

How Does PAXG Work? In-Depth Overview of the Physical Gold Tokenization Mechanism

Aerodrome Tokenomics: How ve(3,3) Powers Base's Most Profitable DEX

How is the price of PAXG determined? Pegging mechanism, trading depth, and influencing factors