The Institutional RWA Infrastructure Taking Shape in Early 2026

tbh what’s happened in institutional RWA tokenization over the last six months is worth looking at closely. The market is approaching $20 billion. Not speculative hype, actual institutional capital deployed on-chain.

I’ve been tracking this space for a while, and the acceleration is wild. Treasuries, private credit, tokenized stocks: all moving to blockchain infrastructure faster than the narrative suggests.

Five protocols emerged as the foundation: Rayls Labs, Ondo Finance, Centrifuge, Canton Network, and Polymesh. They’re not competing for the same customers. Each targets a distinct slice of institutional needs. Banks wanting privacy. Asset managers seeking efficiency. Wall Street firms requiring compliance infrastructure.

This isn’t about which one “wins.” It’s about which Rails institutions choose, and how trillions in traditional assets will actually migrate using them.

The Market Nobody’s Watching Approaches $20 Billion

Three years ago, tokenized RWAs barely registered as a category. Today, approaching $20 billion deployed across Treasuries, private credit, and public equities. Up from the $6-8 billion range in early 2024.

ngl the breakdown is more interesting than the headline number.

Current market snapshot (per rwa.xyz, early January 2026):

• Treasury securities and money market funds: ~$8-9 billion (45-50% of market)

• Private credit: $2-6 billion (fastest-growing from smaller base, 20-30%)

• Public equities: $400+ million (surging, primarily Ondo-led)

Three drivers are accelerating adoption:

Yield arbitrage matters. Tokenized Treasury products deliver 4-6% returns with 24/7 accessibility versus traditional T+2 cycles. Private credit vehicles offer 8-12%. For institutional treasurers managing billions in idle capital, the math is straightforward.

Regulatory frameworks now in place. The EU’s MiCA regulation now enforces across 27 countries. SEC Project Crypto is advancing on-chain securities frameworks. No-Action Letters enabled infrastructure players like DTCC to tokenize assets.

Custody and oracle infrastructure matured. Chronicle Labs processed over $20 billion in total value secured. Halborn completed security audits for major RWA protocols. The plumbing works well enough to meet fiduciary standards.

The challenges remain significant though. Cross-chain fragmentation costs an estimated $1.3 billion annually. Identical assets trade at 1-3% spreads across blockchains because moving capital costs more than the arbitrage is worth. Privacy requirements clash with regulatory transparency demands.

Rayls Labs: Privacy Infrastructure Banks Actually Want

@ RaylsLabs positioned itself as the compliance-first bridge between banking and decentralized finance. Developed by Brazilian fintech Parfin and backed by Framework Ventures, ParaFi Capital, Valor Capital, and Alexia Ventures, it operates as a public-permissioned EVM-compatible Layer 1 designed explicitly for regulated institutions.

I’ve been following the Enygma development for some time now. What matters isn’t the tech specs. It’s the approach. Rayls is solving for what banks actually need, not what DeFi Twitter thinks banks should want.

The Enygma privacy stack:

• Zero-knowledge proofs for transaction confidentiality

• Homomorphic encryption enabling computation on encrypted data

• Native operation across public chain and private institutional networks

• Confidential payments with atomic swaps and embedded delivery-versus-payment

• Programmable compliance with selective disclosure to designated auditors

Real-world deployments include:

• Banco Central do Brasil: CBDC cross-border settlement pilots

• Núclea: Regulated receivables tokenization

• Multiple unnamed node clients: Private DvP workflows

Fresh validation: Rayls announced Halborn security audit completion on January 8, 2026. Institutional-grade security attestation for RWA infrastructure. This matters for banks evaluating production deployment.

The AmFi Alliance targets $1 billion in tokenized assets on Rayls by June 2027, supported by a 5 million RLS token grant. AmFi (Brazil’s largest private credit tokenization platform) brings immediate deal flow with specific milestones phased over 18 months. This is one of the largest institutional RWA commitments to any blockchain ecosystem.

Target market: Banks, central banks, and asset managers requiring institutional-grade privacy. The public-permissioned model restricts validator participation to licensed financial entities while keeping transaction data confidential.

The challenge is demonstrating traction. Without public TVL metrics or announced client deployments beyond pilots, the $1 billion AmFi target by mid-2027 is where this gets tested.

Ondo Finance: Racing to Scale Across Chains

@ OndoFinance executed the fastest institutional-to-retail expansion in RWA tokenization. What started as a Treasury-focused protocol is now the biggest platform in tokenized public equities.

Current metrics (January 2026):

• Total value locked: $1.93 billion

• Tokenized stocks: $400+ million, surpassing milestones (53% market share)

• USDY holdings on Solana: ~$176 million

I tested the USDY product on Solana. The UX is genuinely smooth: institutional Treasuries with DeFi accessibility. That combo is what matters.

Recent momentum: Ondo dropped 98 new tokenized assets on January 8, 2026. Stocks and ETFs spanning AI, EV, and thematic sectors. This isn’t slow rollout. This is moving fast.

Ondo’s planned Q1 2026 launch of tokenized U.S. stocks and ETFs on Solana marks its most aggressive push into retail-friendly infrastructure. The product roadmap targets 1,000+ tokenized assets as the expansion scales.

Sectoral focus:

• AI sector: Nvidia, data center REITs

• Electric vehicles: Tesla, battery manufacturers

• Thematic exposure traditionally locked behind minimum thresholds

Multi-chain deployment strategy:• Ethereum: DeFi liquidity and institutional legitimacy • BNB Chain: Exchange-native users • Solana: Consumer-scale throughput with sub-second finality

ngl Ondo hitting $1.93B TVL while the token price tanked is exactly the signal that matters: protocol growth over speculation. The growth comes from institutional treasuries and DeFi protocols seeking yield on idle stablecoins. TVL increases during Q4 2025 market consolidation show real demand, not just momentum chasing.

By securing broker-dealer custody relationships, completing Halborn security audits, and launching live products across three major chains within six months, Ondo built a lead that competitors are struggling to close. Backed Finance trails significantly at ~$162 million in tokenized assets.

The off-hours challenge: While tokens can transfer continuously, pricing must still reference exchange hours, creating potential arbitrage gaps during U.S. night sessions. Securities laws require rigorous KYC and accreditation verification, limiting the “permissionless” narrative.

Centrifuge: When Asset Managers Actually Deploy Billions

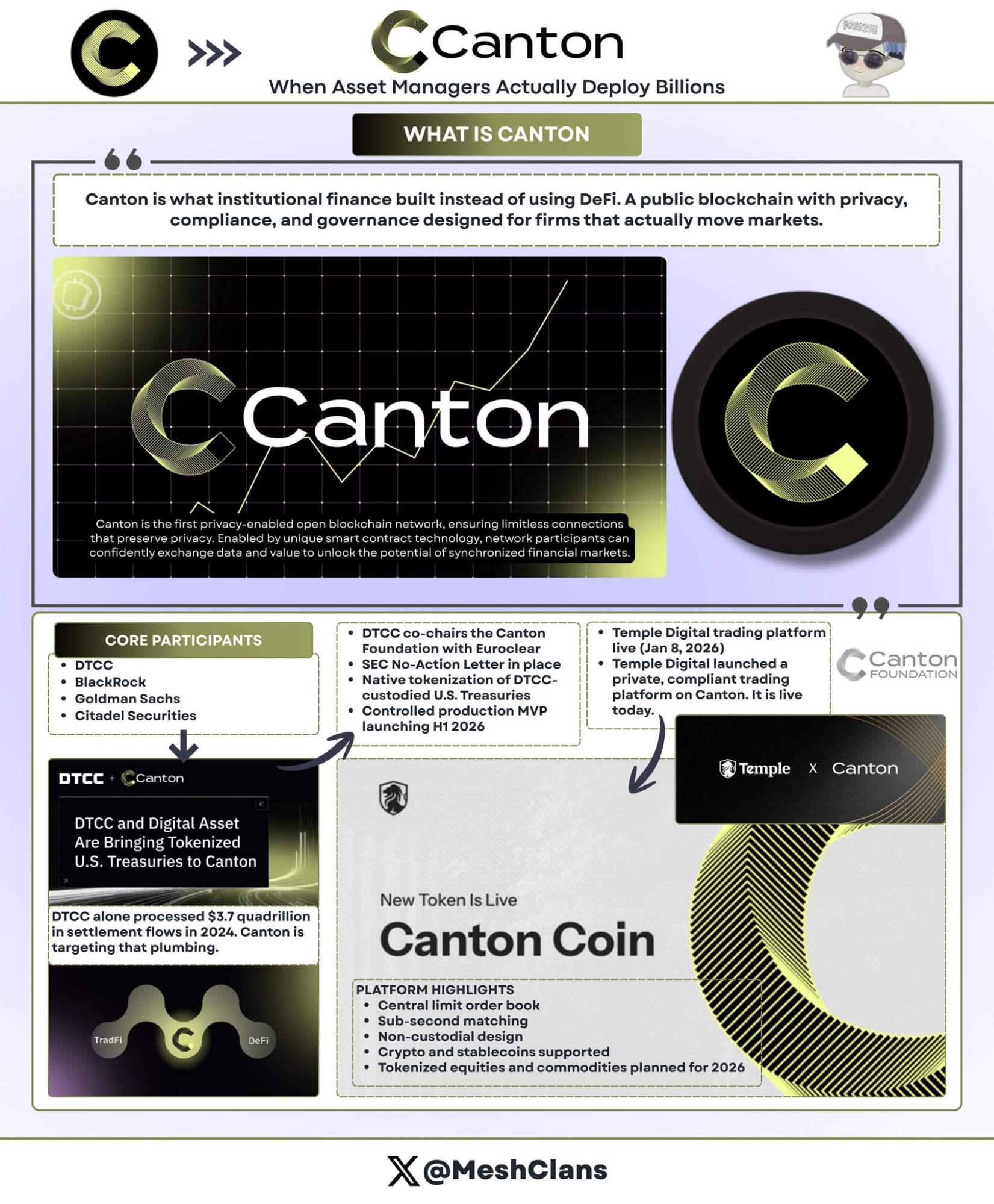

@ centrifuge became the infrastructure standard for institutional-grade private credit tokenization. The protocol’s TVL surged to $1.3-1.45 billion as of December 2025, driven by institutional capital deployment that’s actually happening.

Major institutional deployments:

Janus Henderson partnership ($373 billion AUM global asset manager) • Anemoy AAA CLO Fund: Fully on-chain AAA-rated collateralized loan obligations • Same portfolio managers as $21.4 billion AAA CLO ETF • July 2025 expansion targeting additional $250 million on Avalanche

Grove allocation (Sky ecosystem institutional credit protocol) • $1 billion committed allocation strategy • $50 million deployed as initial anchor capital • Founders from Deloitte, Citigroup, BlockTower Capital, Hildene Capital Management

Chronicle Labs oracle partnership (announced January 8, 2026) • Proof of Asset framework provides cryptographically verified holdings-level data • Transparent NAV calculations, custody verification, compliance reporting • Dashboard accessible to LPs and auditors

I’ve also been tracking the oracle problem too. Chronicle’s approach is the first solution that makes sense for institutional requirements: verifiable data without compromising on-chain efficiency. The January 8 announcement included a video walkthrough showing it works now, not later.

How Centrifuge works differently:

Unlike competitors that wrap off-chain products, Centrifuge tokenizes credit strategies at issuance. The process:

- Issuers structure and manage funds through single transparent workflow

- Institutional investors allocate stablecoins

- Capital flows to borrowers after credit underwriting

- Repayments distribute proportionally to token holders via smart contracts

- APYs range 3.3-4.6% on AAA-rated assets with full transparency

Multi-chain V3 architecture:• Ethereum • Base • Arbitrum • Celo • Avalanche

What matters here? Asset managers needed proof that on-chain credit works for billions in deployment. Centrifuge delivered. The Janus Henderson relationship alone provides multi-billion-dollar capacity.

The protocol’s leadership in industry standards (co-founding the Tokenized Asset Coalition and Real-World Asset Summit) reinforces its position as infrastructure rather than product.

The challenge is scaling beyond anchored capital. While $1.45 billion TVL validates institutional appetite, the 3.8% target APY underperforms DeFi’s historically higher-risk, higher-yield opportunities. Attracting DeFi-native liquidity providers beyond Sky ecosystem allocations is the next hurdle.

Canton Network: Wall Street’s Blockchain Infrastructure

@ CantonNetwork represents institutional blockchain’s answer to DeFi’s permissionless ethos: a privacy-preserving public network backed by Wall Street’s largest firms.

Participants include:

• DTCC (Depository Trust & Clearing Corporation)

• BlackRock

• Goldman Sachs

• Citadel Securities

Canton targets the $3.7 quadrillion in annual settlement flows DTCC processed in 2024. That number isn’t a typo.

The DTCC partnership (December 2025)

The DTCC partnership is massive. This is the backbone of U.S. securities settlement co-chairing Canton’s foundation. That’s not a pilot. That’s infrastructure commitment.

The collaboration, approved via SEC No-Action Letter, enables a subset of DTCC-custodied U.S. Treasury securities to be tokenized natively on Canton with a controlled production MVP launching in H1 2026.

Key details:

• DTCC co-chairs Canton Foundation alongside Euroclear

• Governance leader rather than mere participant

• Initial focus on Treasuries (minimal credit risk, deep liquidity, clear regulatory treatment)

• Post-MVP expansion could encompass corporate bonds, equities, structured products

At first I was skeptical of permissioned blockchains. The DTCC partnership changed my perspective. Not because it’s technically superior, but because it’s infrastructure traditional finance will actually adopt.

Temple Digital launch (January 8, 2026)

Canton’s institutional value proposition crystallized with Temple Digital Group’s January 8 launch of a private trading platform. This went live, not “coming soon.”

Central limit order book with sub-second matching, non-custodial structure. Currently supports cryptocurrencies and stablecoins. Tokenized equities and commodities planned for 2026.

Ecosystem: Franklin Templeton ($828M money market fund), JPMorgan (JPM Coin for DvP settlement).

Canton’s privacy architecture:

Privacy operates at smart contract level using Daml (Digital Asset Modeling Language):

• Contracts specify exactly which parties observe which data

• Regulators access full audit trails

• Counterparties view transaction details

• Competitors and public see nothing

• State updates propagate atomically across network

For institutions accustomed to confidential Bloomberg terminals and dark pools, Canton’s architecture provides blockchain efficiency without exposing trading strategies. Makes sense when you think about it. Wall Street will never adopt transparent public ledgers for proprietary trading.

The network’s 300+ participants demonstrate institutional engagement, though much reported volume likely represents simulated pilot activity rather than production flows. The constraint is velocity: H1 2026 MVP delivery reflects multi-quarter planning cycles. DeFi protocols ship products in weeks.

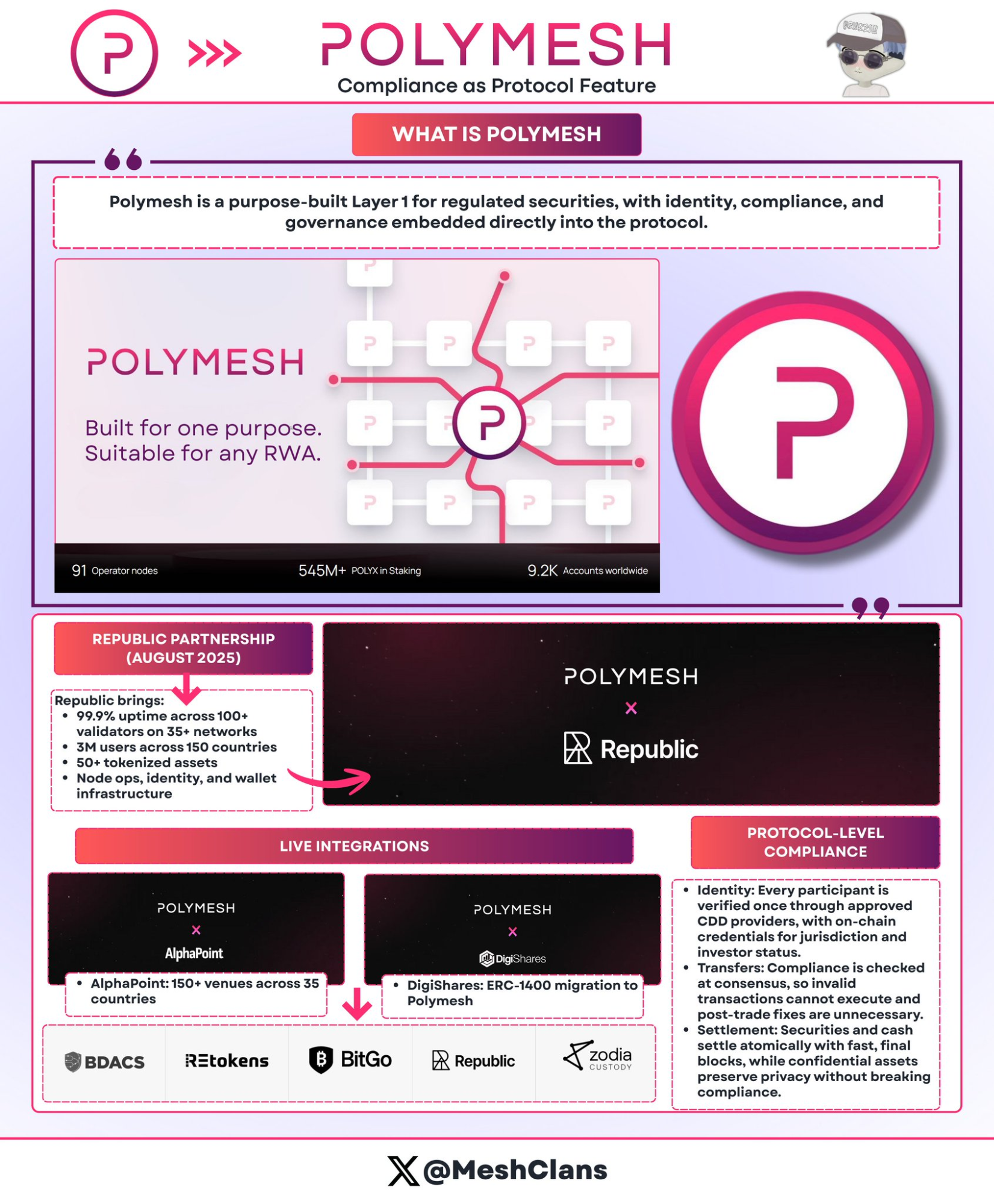

Polymesh: Compliance-Native Securities Blockchain

@ PolymeshNetwork differentiates through protocol-level compliance instead of smart contract complexity. Built specifically for regulated securities, compliance verification happens at consensus, not in custom code.

Core approach:

• Identity verification required at protocol level (permissioned CDD providers)

• Transfer rules embedded in protocol (non-compliant transactions fail at consensus)

• Atomic delivery-versus-payment with six-second finality

Production integrations:

• Republic (August 2025): Private securities offerings

• AlphaPoint: 150+ venues across 35 countries

• Target: Regulated funds, real estate, corporate equity

Benefits: No custom smart contract audits, protocol handles regulatory changes, impossible to execute non-compliant transfers.

Challenge: Standalone chain separates it from DeFi liquidity. The planned Q2 2026 Ethereum bridge aims to fix this. We’ll see if it delivers.

I’ll admit I underestimated compliance-native architecture. For security token issuers drowning in ERC-1400 complexity, Polymesh’s approach makes sense: bake compliance into the protocol, not the contracts.

How These Protocols Segment the Market

The five protocols don’t compete directly because they solve different problems:

Privacy approaches:

• Canton: Daml smart contracts (Wall Street counterparty relationships)

• Rayls: Zero-knowledge proofs (banking-grade mathematical privacy)

• Polymesh: Protocol-level identity (turnkey compliance)

Scale strategies:

• Ondo: $1.93B across three chains, velocity over depth

• Centrifuge: $1.3-1.45B institutional credit, depth over velocity

Target markets:

• Banks/CBDCs → Rayls

• Retail/DeFi → Ondo

• Asset managers → Centrifuge

• Wall Street → Canton

• Security tokens → Polymesh

imo this segmentation matters more than people realize. Institutions aren’t picking “the best blockchain.” They’re choosing infrastructure that solves their specific regulatory, operational, and competitive needs.

The Problems Nobody Solved Yet

Cross-chain fragmentation is expensive: Estimated $1.3-1.5 billion in annual costs. Identical assets trade at 1-3% spreads across blockchains because bridging costs more than arbitrage is worth. Projected 2030 cost if unresolved: $75+ billion.

This is the problem I worry about most. You can build the best tokenization infrastructure, but if liquidity fragments across incompatible chains, the efficiency gains disappear.

Privacy vs transparency: Institutions need confidentiality. Regulators demand auditability. Multi-party scenarios (issuers, investors, rating agencies, regulators, auditors) each need different visibility levels. No perfect solution exists.

Regulatory fragmentation: EU has MiCA (27 countries). US requires case-by-case No-Action Letters (months-long). Cross-border flows face jurisdictional conflicts.

Oracle risks: Tokenized assets depend on off-chain data. If data providers get compromised, on-chain representations reflect false realities. Chronicle’s Proof of Asset framework helps, but risk remains.

fr these aren’t small problems. They’re fundamental infrastructure challenges that every protocol is wrestling with differently. No one has perfect solutions yet.

The Path to $100 Billion: 2026 Catalysts

2026 catalysts to watch:

- Ondo’s Solana launch (Q1 2026)

• Tests whether retail-scale distribution creates sustainable liquidity

• Success metric: 100,000+ holders demonstrating genuine demand

- Canton’s DTCC MVP (H1 2026)

• Validates blockchain settlement for Treasury securities

• If successful: Multi-trillion-dollar flows could move to on-chain infrastructure

- U.S. CLARITY Act passage

• Provides regulatory certainty

• Enables institutional allocators currently sidelined to deploy capital

- Centrifuge’s Grove deployment

• $1 billion allocation completing throughout 2026

• This tests institutional credit tokenization with real capital

• Successful execution without credit events builds asset manager confidence

Market projections:

• 2030 target: $2-4 trillion in tokenized assets

• Growth required: 50-100x from current $19.7 billion

• Assumes: regulatory stability, interoperability readiness, no major institutional failures

Growth by sector:

• Private credit: $2-6B currently → $150-200+ billion by 2030 (from smaller base, highest growth rate)

• Tokenized Treasuries: Potential $5+ trillion if money market funds migrate on-chain

• Real estate: Projected $3-4 trillion (depends on property registries adopting blockchain-compatible titling)

The $100 billion milestone:

Likely arrival: 2027-2028

Projected breakdown:

• Institutional credit: $30-40B

• Treasuries: $30-40B

• Tokenized stocks: $20-30B

• Real estate/commodities: $10-20B

This requires approximately 5x growth from current levels. Aggressive but plausible given Q4 2025’s institutional momentum and upcoming regulatory clarity.

Why These Five Protocols Matter

The institutional RWA landscape in early 2026 reveals something unexpected: there’s no single winner because there’s no single market.

And honestly? That’s exactly how infrastructure should develop.

Each protocol solves a different problem:

• Rayls → Banking privacy

• Ondo → Tokenized equity distribution

• Centrifuge → Asset manager on-chain deployment

• Canton → Wall Street infrastructure migration

• Polymesh → Securities compliance simplification

The market’s growth from $8.5 billion in early 2024 to $19.7 billion shows real demand beyond speculation.

What institutional players want:

• Treasurers: Yield and operational efficiency

• Asset managers: Reduced distribution costs, expanded investor bases

• Banks: Infrastructure that meets compliance requirements

The next 18 months test these platforms:

• Ondo’s Solana launch → Tests retail scalability

• Canton’s DTCC MVP → Tests institutional settlement

• Centrifuge’s Grove deployment → Tests credit tokenization with real capital

• Rayls’ $1B AmFi target → Tests privacy infrastructure adoption

Execution over architecture. Results over roadmaps. That’s what matters now.

Traditional finance is beginning a years-long migration on-chain. These five protocols provide the infrastructure institutional capital needs: privacy layers, compliance frameworks, and settlement infrastructure. Their success determines not whether tokenization happens (regulatory momentum makes that inevitable) but how: as efficiency improvements within existing structures, or as something that replaces the intermediation models finance has used for centuries.

The infrastructure choices institutions make in 2026 will define this for the next decade.

Track these catalysts through 2026. This is when we’ll see which infrastructure actually works. The job’s not done, not even close. But institutions are making their choices now, and tbh it’s moving faster than the narrative suggests.

Key milestones to watch:

• Q1: Ondo Solana launch (98+ stocks live)

• H1: Canton DTCC MVP (Treasury tokenization with Wall Street infrastructure)

• Ongoing: Centrifuge Grove $1B deployment, Rayls AmFi buildup

Trillions incoming.

NFA.

Disclaimer:

- This article is reprinted from [MeshClans]. All copyrights belong to the original author [MeshClans]. If there are objections to this reprint, please contact the Gate Learn team, and they will handle it promptly.

- Liability Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute any investment advice.

- Translations of the article into other languages are done by the Gate Learn team. Unless mentioned, copying, distributing, or plagiarizing the translated articles is prohibited.

Related Articles

What is Plume Network

What Are Crypto Narratives? Top Narratives for 2025 (UPDATED)

In-Depth Analysis of BlackRock’s BUIDL Fund: How It Reshapes the RWA Landscape

ONDO, a Project Favored by BlackRock

Reshaping Web3 Community Reward Models with RWA Yields