How Does Rayls Work? From Private Banking Chains to DeFi Liquidity

Rayls connects banking systems with DeFi liquidity through a combined architecture of private chains, a public chain, and privacy nodes. Financial institutions can manage accounts, transactions, and compliance data within private networks, while using Rayls Public Chain and cross chain protocols to bring tokenized deposits, stablecoins, and real world assets (RWA) into open on-chain markets.As stablecoins, RWA (real world assets), and institution grade DeFi markets grow rapidly, more banks and financial institutions are asking how they can safely enter the on-chain financial system. Traditional financial institutions usually operate under strict requirements for data management, identity verification, and regulatory compliance, while open public chains emphasize transparency and permissionless access. These two systems have long differed at the most fundamental level. Allowing traditional financial assets to enter on-chain markets while preserving privacy and compliance has become a core challenge for institutional blockchain development.

Rayls emerged as institution grade blockchain infrastructure in response to this need. Its goal is not simply to replicate a traditional consortium chain, but to build a hybrid architecture that can work with banking systems, private financial networks, and the open DeFi ecosystem at the same time.

What Is the Core Architecture of Rayls?

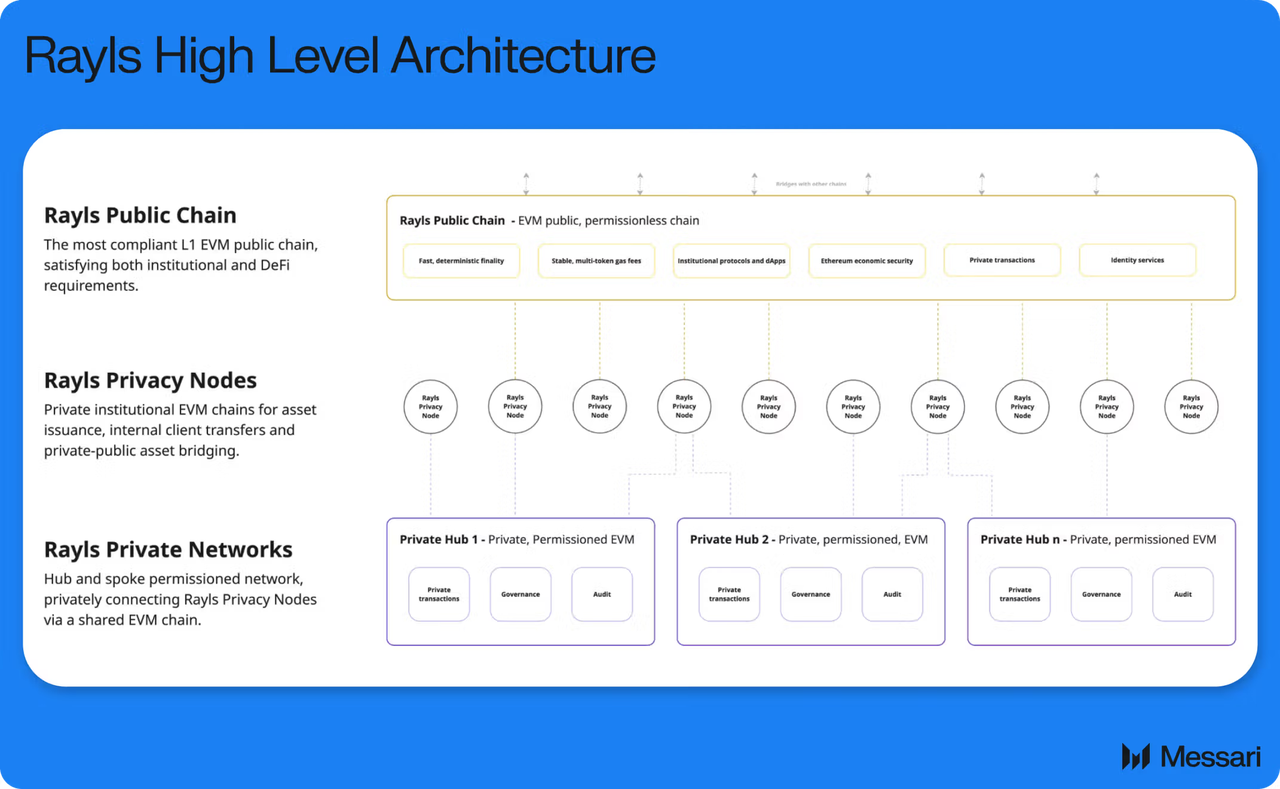

The Rayls network is mainly composed of three parts: institutional private chains, known as Subnets, Rayls Public Chain, and Privacy Nodes.

Institutional private chains are designed mainly for internal use by banks and financial institutions. They handle account data, transaction records, and compliance information. Unlike traditional public chains, this part of the network is not fully open to everyone. Access is limited to authorized participants.

Rayls Public Chain is responsible for public settlement and for connecting with the open ecosystem. It uses an EVM compatible architecture, which means it can support Solidity smart contracts and remain compatible with public chain ecosystems such as Ethereum.

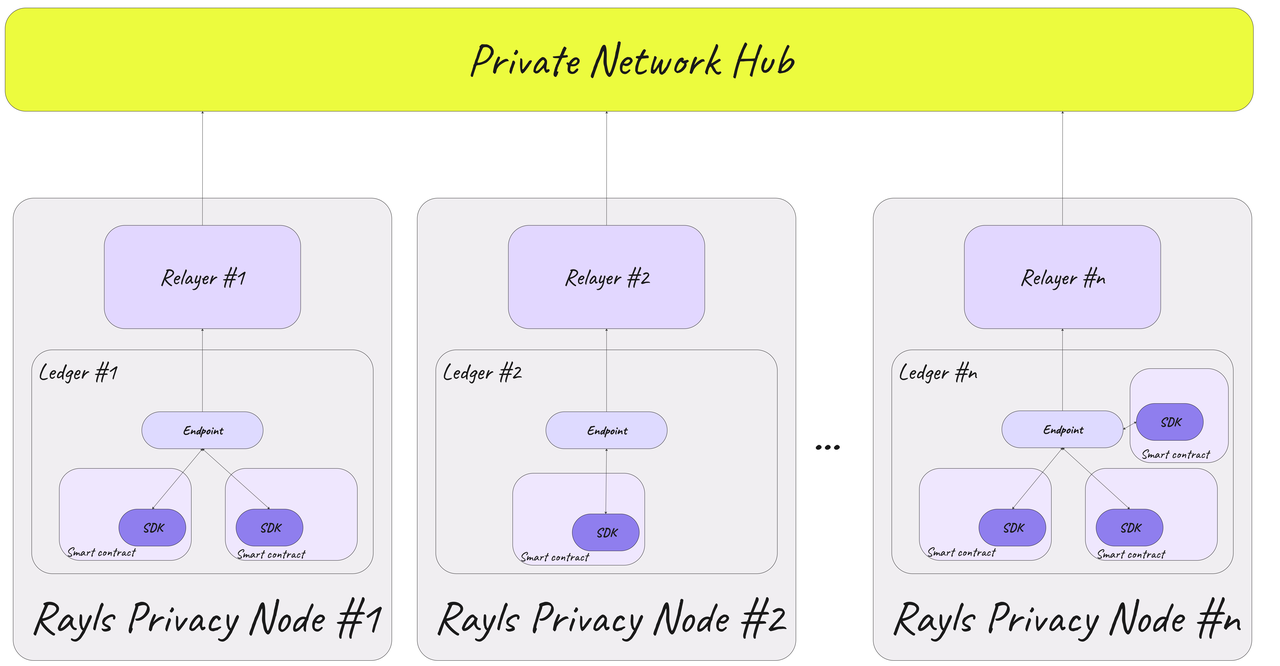

Privacy Node is one of the key modules in the entire system. Its role is to protect sensitive financial data. Some transaction and identity information is not exposed directly on the public network, but is instead verified and communicated through the privacy layer.

The central purpose of this architecture is to let institutions maintain control over their data while still gaining access to open on-chain liquidity.

How Do Banks Connect to the Rayls Network?

When a bank or financial institution connects to Rayls, it usually begins by deploying its own private network environment.

At this stage, the institution can connect its existing account system, payment system, or asset management platform to the Rayls network. Because the private chain supports permission control, only authorized participants can access the relevant data.

Banks can also deploy digital asset management logic within the private network, such as tokenized deposits, digital bonds, or stablecoin issuance systems. Compared with directly exposing data on an open public chain, this model is better aligned with the financial industry’s requirements for privacy and regulation.

At the same time, the institution’s deployed Privacy Node handles encrypted communication, identity verification, and on-chain data synchronization, creating a secure connection between the private network and the public network.

How Are Tokenized Deposits Created?

Tokenized deposits are one of the important applications in the Rayls ecosystem. In essence, they map traditional bank deposits into on-chain digital assets.

After a user deposits fiat funds in a bank, the bank can create the corresponding on-chain token within its private network. For example, a 1 dollar deposit can be mapped to 1 on-chain digital credential. This asset usually remains under the supervision of the banking system and maintains a corresponding relationship with the real deposit.

Compared with traditional stablecoins, tokenized deposits place more emphasis on integration with bank account systems and regulatory frameworks. The asset does not completely separate from the financial institution. Instead, it becomes a digital representation within a regulated environment.

Once created, the asset can remain within the private network. It can also enter a broader on-chain market through Rayls Public Chain after regulatory conditions are met.

How Do Assets Enter Rayls Public Chain?

When an institution wants its assets to gain broader liquidity, the relevant digital assets can enter Rayls Public Chain through cross chain and mapping mechanisms.

During this process, the Privacy Node verifies the asset source, account permissions, and compliance status. Only assets that meet the required rules can enter the public network.

After entering the Public Chain, the assets can interact with on-chain smart contract systems. For example, users can use tokenized deposits for on-chain payments, asset settlement, or other financial protocols.

Because Rayls uses an EVM compatible architecture, these assets can also connect to the existing Ethereum tool ecosystem, including wallets, smart contract frameworks, and certain DeFi applications.

This structure gives banking assets the ability to circulate and be combined within an open on-chain environment for the first time.

How Does Rayls Connect to DeFi Liquidity?

Traditional financial assets have long lacked a direct way to connect with DeFi markets. One of Rayls’ core values is that it builds this liquidity bridge.

After assets enter Rayls Public Chain, they can connect further with other on-chain protocols. For example, certain institutional assets can be used for on-chain payments, liquidity pools, or digital asset settlement.

Compared with the traditional consortium chain model, Rayls places greater emphasis on the composability of open finance. Assets do not remain only inside a closed system. They can also interact with broader DeFi infrastructure.

How Does Rayls’ Cross Chain Mechanism Work?

Institutional financial networks usually do not rely on a single blockchain, which makes cross chain interoperability a key part of Rayls.

Rayls supports an EVM compatible environment and can communicate with other blockchains through cross chain protocols. This means institutional assets can not only exist within the Rayls network, but also move between different chains.

For example, some tokenized assets can move from an institutional private chain into Rayls Public Chain, and then connect further with other open blockchain ecosystems. During this process, the Privacy Node handles permission verification and encrypted communication, preventing sensitive data from being directly exposed on the public network.

Compared with traditional cross chain bridge models, Rayls focuses more on regulation and identity management, so its cross chain logic is closer to a financial network interoperability layer.

Conclusion

Through its combined architecture of private chains, a public chain, and privacy nodes, Rayls provides banks and financial institutions with a blockchain infrastructure solution that balances compliance, privacy, and open liquidity.

Rayls’ core operating process includes institutional private network deployment, tokenized asset issuance, privacy verification, cross chain communication, and access to on-chain liquidity. Compared with traditional consortium chains, Rayls places greater emphasis on connecting institutional assets with the open DeFi ecosystem.

FAQs

What Parts Make Up Rayls’ Core Architecture?

It mainly includes institutional private chains, known as Subnets, Rayls Public Chain, and Privacy Nodes.

How Does Rayls Protect Financial Data Privacy?

Rayls uses Privacy Nodes to perform encrypted verification and permission control for sensitive data, preventing key financial information from being directly exposed on public networks.

What Are Tokenized Deposits?

Tokenized deposits map bank deposits into on-chain digital assets, allowing traditional financial funds to enter the blockchain ecosystem.

Does Rayls Support EVM?

Yes. Rayls uses an EVM compatible architecture, so it can work with Solidity smart contracts and the Ethereum tool ecosystem.

How Does Rayls Connect to DeFi?

Institutional assets can enter open on-chain markets through Rayls Public Chain and cross chain protocols, then interact with DeFi protocols.

Related Articles

In-depth Explanation of Yala: Building a Modular DeFi Yield Aggregator with $YU Stablecoin as a Medium

Sui: How are users leveraging its speed, security, & scalability?

How Does PAXG Work? In-Depth Overview of the Physical Gold Tokenization Mechanism

What Is a Yield Aggregator?

Dive into Hyperliquid